The Higher Education Loans Board (HELB) remains the single most critical funder of higher education dreams in Kenya. As thousands of graduates enter the workforce each year, their commitment to responsible HELB repayment in Kenya directly sustains the revolving fund for future students.

In 2025, the landscape of loan servicing is defined by an aggressive shift towards digital convenience and stricter compliance. This comprehensive guide provides everything you need to know about navigating your HELB repayment in Kenya—from the new eCitizen payment gateway and policy changes to securing your final clearance certificate.

I. Understanding HELB: The Revolving Fund and Your Obligation

A. What is HELB and Why Does My Repayment Matter?

HELB is a statutory body established by the HELB Act, Cap 213A, of the Laws of Kenya. Its mandate is dual: to source, manage, and recover loans. Your HELB repayment in Kenya is not merely the settlement of a personal debt; it is a direct investment into the nation’s human capital. The HELB model operates as a revolving fund. This means that money repaid by past beneficiaries is recycled to finance the education of the current generation of students.

- The Revolving Fund Fact: For every Ksh 100 recovered from loanees, a significant percentage goes directly back into loan disbursements. HELB estimates that loan recoveries contribute billions of shillings annually, directly reducing reliance on the National Exchequer.

- The National Mandate: The success of the government’s Higher Education Financing (HEF) Model, launched to address increased student enrollment, hinges on the robust recovery of loans.

The importance of timely HELB repayment in Kenya cannot be overstated. When a borrower defaults, it creates a funding gap that risks denying a deserving high school graduate the opportunity to attend university or a TVET college.

B. What Types of HELB Loans Require Repayment?

The repayment obligation applies to all recoverable funds received during your time in tertiary education. It is crucial to know exactly which funds you need to service.

The categories include:

- Undergraduate Loans: The most common form of assistance for students admitted under the Government-Sponsored Programme (GSP) in local universities.

- TVET Loans: Financial support specifically tailored for students pursuing courses in Technical and Vocational Education and Training institutions.

- Jielimishe Loans: Loans for salaried employees pursuing postgraduate or advanced degree programs.

- Partner Funds: Loans or bursaries managed by HELB on behalf of government agencies or corporate partners (e.g., Afya Elimu Loan).

Note on Non-Repayable Funds: Bursaries and Scholarships, which are typically allocated based on need through the Means Testing Instrument (MTI), are generally non-repayable portions of aid.

C. The Legal Obligation and Contract

When you applied for your HELB loan, you signed a contract with the Board. This contract, governed by the HELB Act, stipulates the terms of repayment, including the interest rate, the commencement date, and the consequences of default.

- Key Fact: According to the HELB Act, a loanee is legally bound to inform the Board of their contact address and employment status and commence loan repayment within the stipulated time frame. This is a legally enforceable debt.

II. When Exactly Should You Begin HELB Repayment in Kenya?

Understanding the official start date for your HELB repayment in Kenya is crucial to avoid steep, unnecessary penalties. Many graduates mistakenly believe they only need to start paying once they secure formal employment. This is a common and costly error.

A. What is the Statutory Grace Period?

The repayment clock for your HELB loan begins ticking one (1) year after you officially complete your studies. HELB legally defines this as the date of your graduation. This 12-month period is a grace period intended to give you time to adjust and find employment.

| Repayment Scenario | When Obligation Starts | Statutory Implication |

| Standard Graduate | 12 months after your date of graduation (the 13th month). | Mandatory monthly payments must commence to avoid penalties. |

| Unemployed Graduate | The 13th month after graduation. | Must officially apply for a Jobless Moratorium to pause penalty accrual. |

| Employed During Grace Period | Anytime before the 13th month. | Encouraged to begin early to minimize accrued interest and principal. |

It is essential to mark your calendar for the 13th month after your graduation. Missing this deadline, even by one day, is what triggers the default penalty.

B. What is the Current Interest Rate and Penalty?

The statutory charges on your loan are structured to motivate early and consistent HELB repayment in Kenya. These charges are dual-layered:

- Interest Rate: A flat rate of 4% per annum is charged on the disbursed loan amount. This interest accrues from the date of the first disbursement until the loan is settled.

- Penalty for Default: This is the most financially devastating charge. A punitive fine of Ksh 5,000 is levied per month on the outstanding loan balance for failure to commence HELB repayment in Kenya after the grace period expires.

- Case Study Example: Consider a loanee who owes Ksh 250,000 and defaults for three years (36 months).

- Penalty Calculation: 36 months $\times$ Ksh 5,000/month = Ksh 180,000 in penalties alone!

- This amount is independent of the 4% annual interest, illustrating why communication with HELB and applying for deferment is vital.

C. Deferment for Unemployment or Further Studies (The Jobless Moratorium)

The only legal mechanism to temporarily halt the accrual of the punitive Ksh 5,000 monthly penalty is to apply for a Jobless Moratorium or Deferment.

- Who Qualifies? Graduates who are currently unemployed or are pursuing further education (e.g., Master’s or PhD) and cannot afford HELB repayment in Kenya.

- The Process:

- Log into the HELB portal.

- Fill out the formal application for Moratorium.

- Attach supporting documents, such as your Graduation Certificate and a signed affidavit confirming your unemployment status (or admission letters for those pursuing further studies).

- Duration and Renewal: This deferment is usually granted for a specific, renewable period (e.g., 12 or 24 months). If you are still unemployed after this period, you must re-apply to prevent penalties from restarting.

Crucial Advice: Never assume that HELB knows your employment status. The responsibility lies solely with the loanee to inform the Board, especially if they cannot begin their HELB repayment in Kenya as scheduled.

Digital Payment Methods: How to Pay Your HELB Loan in 2025

The process for HELB repayment in Kenya has been fully digitized, ensuring transactions are instant, verifiable, and seamlessly integrated with the national payment system. The focus in 2025 is on reducing cash-based payments and promoting efficiency via the eCitizen platform.

A. How Do I Pay HELB Using M-PESA and eCitizen? (Featured Snippet Optimization)

The easiest and most common way to facilitate your HELB repayment in Kenya is through the M-PESA mobile money service. The transaction is immediately routed through the government’s consolidated payment gateway.

Step-by-Step M-PESA Guide:

- Generate a Payment Instruction: Log into the HELB Mobile App or dial the USSD code *642#. Navigate to the Loan Repayment section.

- Request Amount: Enter the specific amount you wish to pay and confirm. This step generates an eCitizen Invoice/Reference Number linked to your National ID.

- Go to M-PESA: Open your M-PESA menu and select Lipa na M-PESA.

- Select Paybill: Choose the Paybill option.

- Enter Business Number: Use the official HELB Business Number 200800.

- Enter Account Number: Use your National ID Number as the account number for accurate allocation.

- Enter Amount & PIN: Key in the payment amount (matching the invoice) and your M-PESA PIN to confirm.

- Confirmation: You will receive instant SMS confirmations from M-PESA and the eCitizen platform. The payment will reflect on your HELB statement shortly.

This digital process eliminates delays and ensures instant allocation, a significant improvement over manual bank deposits.

B. Repayment via Employer Check-off System

For formally employed graduates, the employer deduction system is the most reliable method for consistent HELB repayment in Kenya.

- How it Works: The loanee formally notifies their employer, and the employer takes over the responsibility of deduction and remittance. This is done through the HELB Employer Portal.

- Deduction Rate: While the repayment amount is negotiated with HELB, a common statutory deduction is 15% of the loanee’s basic monthly salary.

- Employer Role: The employer acts as a vital agent for HELB, deducting the funds and submitting the remittance list and payment to HELB by the 15th day of the following month.

Tip for Employees: Always verify with your HR or payroll department that the correct deduction is being made and that the funds are being remitted on time to avoid unexpected penalties on your account.

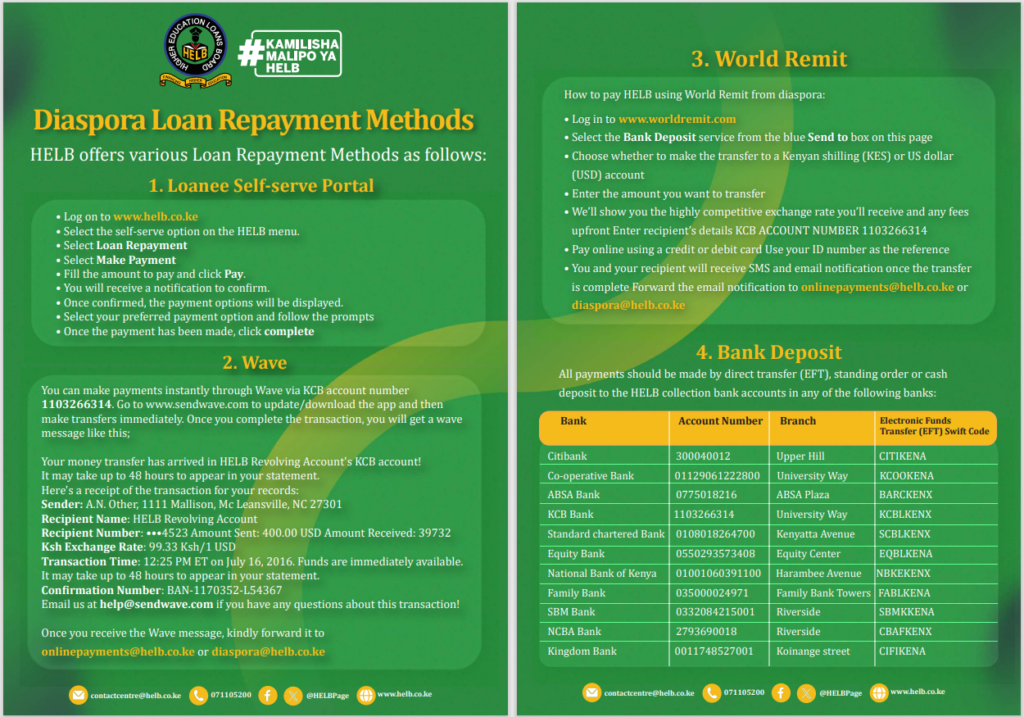

C. Diaspora Repayment Solutions and Bank Transfers

HELB has established specialized channels for loanees working outside Kenya and those preferring traditional banking methods.

- Diaspora Repayment: Kenyans abroad must use the dedicated HELB Diaspora Repayment Portal at repay.helb.co.ke/diaspora. This platform facilitates payments using major foreign currencies (USD, GBP, EUR) via secure international payment methods, including SWIFT transfers or authorized global partners.

- Bank Transfers: While M-PESA is preferred, you can still utilize bank services for HELB repayment in Kenya. This usually involves generating a payment slip or invoice from the HELB portal and depositing the amount directly into HELB’s dedicated accounts at partner banks like Equity, KCB, or Co-operative Bank. This method is often preferred for large lump-sum payments.

Data Fact: The integration of HELB payments with the eCitizen platform and mobile money significantly reduced the time taken for payment allocation from days to minutes, greatly benefiting loanees tracking their compliance.

IV. HELB Policy Updates and Enforcement in 2025

The year 2025 is marked by an increased push for financial accountability across all government agencies. For HELB repayment in Kenya, this translates to updated policies and enhanced enforcement mechanisms aimed at tightening the revolving fund’s sustainability.

A. What is the HELB and KRA Data Synchronization?

One of the most significant policy shifts involves the enhanced data sharing framework between HELB and the Kenya Revenue Authority (KRA). This integration is central to HELB’s strategy to tackle defaulters who are gainfully employed but evade payment.

- The Goal: To achieve a unified citizen financial profile. By cross-referencing National ID and KRA Personal Identification Number (PIN) data, HELB can accurately determine the employment status and income streams of loanees.

- Targeting the Self-Employed: This is particularly crucial for tracking graduates in the vast informal sector (jua kali) and those running private businesses. Previously, these individuals were difficult to track outside the formal check-off system.

- Compliance Drive: The synchronization allows HELB to send targeted, verifiable notices to non-compliant loanees, backed by credible employment data, significantly increasing the pressure for HELB repayment in Kenya.

B. Are There Penalty Waivers or Amnesty Programs in 2025?

HELB has historically relied on penalty waiver campaigns to encourage massive lump-sum payments and bring chronic defaulters back into the repayment system. These programs are expected to continue in 2025.

| Campaign Feature | Description | Benefit to Loanees |

| 100% Penalty Waiver | Announced periodically (often towards the end of the financial year). | All accumulated penalties (Ksh 5,000 per month) are waived if the loanee clears the outstanding principal balance. |

| Principal Focus | These campaigns prioritize the recovery of the core loan amount. | Loanees save potentially hundreds of thousands of shillings in penalties, enabling them to clear the debt quickly. |

| Strategic Use: | HELB uses these waivers as a time-bound incentive for loanees to formalize their HELB repayment in Kenya. |

Expert Tip: Loanees with large penalty accumulations should actively monitor official HELB communication (website, major newspapers) for the announcement of these campaigns. Clearing the principal during a waiver period is the fastest and cheapest way to obtain a Clearance Certificate.

C. How Will the Future Income-Based Repayment (IBR) Affect HELB?

While not fully operational in 2025, the government and HELB are actively discussing a shift toward an Income-Based Repayment (IBR) model, a massive policy change.

- The IBR Concept: Instead of a fixed repayment schedule, the monthly contribution would be calculated as a set percentage of the borrower’s verifiable income, often only kicking in when income exceeds a specific minimum threshold.

- The Need for IBR: This policy aims to address the plight of low-income earners, gig workers, and the unemployed, making HELB repayment in Kenya fairer and more manageable. It acknowledges that graduates earn different salaries and experience varying periods of unemployment.

- Current Status: Implementing IBR requires significant legal amendments to the HELB Act and robust technological infrastructure (likely relying heavily on the KRA data synchronization mentioned above) to verify income accurately. It remains a key policy objective for the near future.

V. Penalties, Defaulters, and Enforcement

The consequence of failing to prioritize HELB repayment in Kenya extends far beyond a simple debt balance. HELB is legally empowered to pursue various punitive and legal actions against loanees who deliberately default, making compliance a necessity for professional life in Kenya.

A. What are the Consequences of Defaulting on HELB Repayment in Kenya?

The immediate and long-term consequences of defaulting are severe, often impacting a loanee’s ability to access essential financial and professional services:

- Credit Reference Bureau (CRB) Listing: This is the most common enforcement tool. Your name will be listed with the CRB as a defaulter, severely damaging your credit score.

- Impact: A negative CRB listing prevents you from accessing loans, credit cards, and mortgages from commercial banks, Saccos, and mobile lending platforms. It essentially restricts your participation in the formal financial economy.

- Legal Action and Prosecution: The HELB Act provides the Board with the power to initiate civil and criminal proceedings against chronic defaulters.

- Fact: Section 15(2) of the Act states that a loanee who neglects or refuses to satisfy the repayment requirements is guilty of an offense and liable to a fine or imprisonment. While imprisonment is rare, legal notices and court summons are not.

- Guarantor Liability: If the loanee cannot be traced or refuses to pay, HELB is legally entitled to pursue the original guarantors who co-signed the loan application. This transfers the entire financial burden and accrued penalties to them.

- Withholding Clearance: Perhaps the biggest barrier for job seekers is the inability to obtain the mandatory HELB Clearance Certificate, which is required by most public and many large private sector employers as a condition of employment.

B. What is the Role of the CRB and How Does Listing Affect You?

The CRB acts as a gatekeeper for credit information. HELB regularly submits the names of non-performing loanees for listing.

- The Power of Listing: The listing impacts your financial reputation for years, even after the debt is settled, underscoring why preventing a default is easier than recovering from one.

- Case Study Insight: A survey found that over 60% of job applicants reported being asked to provide their HELB status before receiving a job offer, illustrating the real-world impact of compliance.

C. Penalty Relief: What If I Have Massive Arrears?

If you have accrued substantial penalties (often exceeding the principal amount), your focus must be on obtaining a penalty waiver.

- Payment Plan Negotiation: You can formalize your HELB repayment in Kenya by visiting a HELB office and negotiating a structured payment plan. Once this is signed and the first installment is paid, the Ksh 5,000 monthly penalty is usually frozen, allowing you to pay down the principal and remaining interest.

- Waiver Campaigns: As noted in Section IV, taking advantage of a 100% Penalty Waiver Campaign is the most effective way to eliminate crippling arrears, provided you can raise the outstanding principal sum.

Actionable Tip: If you receive a default notice or legal communication from HELB, respond immediately. Demonstrating willingness to repay is the single most important factor in securing leniency and a favorable payment plan.

VI. Obtaining Your HELB Clearance Certificate

The HELB Clearance Certificate is the ultimate proof that you have fully settled your student loan obligation. It serves as a vital document for various professional milestones in Kenya and is the ultimate goal of consistent HELB repayment in Kenya.

A. What is the Clearance Certificate and Why Do I Need It?

The Clearance Certificate is a formal document issued by the Board that certifies a loanee has fully repaid their loan principal, interest, and any applicable charges to a zero balance.

It is indispensable for several reasons:

- Professional Requirement: Most public sector organizations (Government Ministries, Parastatals, County Governments) and large private companies in Kenya require the HELB Clearance Certificate as part of the recruitment or promotion process.

- Credit Access: It confirms your financial standing and removes any negative CRB listing related to the loan, restoring your access to formal credit facilities.

- Legal Finality: It provides the loanee with legal finality, absolving them and their guarantors of any future liability concerning the specific loan settled.

B. Clearance Certificate vs. Compliance Certificate: A Key Distinction

It is crucial for graduates managing their HELB repayment in Kenya to understand the difference between the two main certificates issued by the Board:

| Certificate Type | Loan Status | Purpose and Validity |

| Clearance Certificate | Fully Repaid (Ksh 0.00) | Permanent and final proof of debt settlement. Required for top jobs. |

| Compliance Certificate | Actively Repaying | Issued when the loanee is meeting their agreed-upon monthly repayments. Typically valid for a limited period (e.g., 1 year) and is renewable. |

Fact: If you are still repaying your loan, you apply for a Compliance Certificate to show potential employers you are a responsible borrower, but only the Clearance Certificate proves the debt is completely settled.

C. Step-by-Step Guide to Applying for Final Clearance

Once you believe you have fully completed your HELB repayment in Kenya, follow this structured process to obtain your final certificate:

- Verify Zero Balance (Crucial Step): Log into your HELB self-service portal (or the HELB Mobile App) and confirm that your Outstanding Balance is exactly Ksh 0.00. Even a few shillings of accrued interest can prevent the certificate from being issued.

- Apply Online: Navigate to the Loan Recovery Enquiry/Clearance Section on the HELB online portal.

- Submit Request: Fill out the formal application requesting the issuance of the Clearance Certificate. The system typically verifies the loanee’s status against all outstanding loans (Undergraduate, TVET, etc.).

- HELB Verification Period: The Board’s team undertakes a final, internal audit of the account. This process usually takes between 7 to 14 working days to ensure all remittances, including the final interest accrual, have been fully processed.

- Download Certificate: Upon successful verification, a notification is sent, and the final, downloadable, and verifiable HELB Clearance Certificate is made available on your online portal.

Note on Final Interest: Due to the 4% annual interest rate, it is common for a small amount of residual interest to accrue between your final payment and the application date. Expert Advice: Overpay by a small margin (e.g., Ksh 500) on your final installment to buffer against this last-minute interest accrual and speed up the process.

VII. HELB and Employers: Compliance and Penalties

The employer plays a mandatory and legally defined role in the process of HELB repayment in Kenya. The law treats the employer as an agent of the Board, meaning they have explicit obligations and face significant penalties for non-compliance.

A. What are the Statutory Obligations of Employers in Kenya?

According to Section 16 of the HELB Act (Cap 213A), every employer, whether in the public or private sector, must facilitate the recovery of the loan. This means the employer is legally bound to:

- Identify Loanees: Within three months of hiring a new employee, the employer must inquire from the employee whether they are a HELB loanee. If they are, the employer must inform HELB in writing immediately, providing the employee’s details (name, ID number, and employment date).

- Deduct Monthly: The employer must effect the required deduction amount from the loanee’s salary monthly, using the “check-off system.” This deduction is typically calculated on the loanee’s basic pay.

- Remit Timely: The deducted funds, along with a schedule detailing the names and amounts for each loanee, must be remitted directly to HELB by the 15th day of the following month.

- Fact: Many Human Resource (HR) software and payroll systems in Kenya (e.g., in use across major companies and government agencies) now have dedicated modules to ensure accurate calculation and timely remittance of HELB repayment in Kenya alongside statutory deductions like PAYE and NSSF.

B. Employer Penalties for Non-Compliance

The Act prescribes stiff penalties for employers who fail to comply with the remittance rules. These measures are in place to ensure the revolving fund is not hampered by administrative laziness or negligence.

- Financial Penalty: Under Section 17 of the HELB Act, any employer who fails to deduct or remit the required HELB repayment in Kenya on time is liable to pay a sum equivalent to 5% of the un-remitted amount for each month or part thereof that the payment remains outstanding.

- Implication: This penalty is an addition to the principal amount due. The employer, not the employee, becomes liable for this fine.

- Legal Action: HELB is empowered to take legal action against employers who chronically fail to comply with deduction and remittance requirements.

| Employer Compliance Scenario | Legal Consequence | Responsibility |

| Failure to Notify HELB of Loanee Hiring | Formal query and potential fine under the Act. | Employer’s HR Department |

| Late Remittance of Deducted Funds | 5% penalty per month on the unremitted sum. | Employer’s Finance Department |

| Non-Deduction of Scheduled Payment | Employer becomes liable for the penalty and the un-deducted principal. | Employer |

Quote: “The employer acts as the legal guarantor for the monthly remittance. Failure to deduct is not an employee’s problem; it’s an employer’s legal liability.” – HELB Compliance Officer, in a public statement.

C. What Should Employees Do to Ensure Compliance?

As a loanee, you are responsible for making sure your employer fulfills their statutory duties concerning your HELB repayment in Kenya.

- Verification: Upon employment, immediately confirm with your HR department that they have been informed of your loanee status and that the deduction has commenced.

- Statement Check: Regularly check your HELB online statement (at least quarterly) to ensure that the amounts deducted from your payslip match the amounts remitted to your HELB account.

- Action: If a discrepancy is noted, raise the issue formally with your employer’s HR/Payroll department first. If the issue is not resolved, formally notify HELB of the non-compliance.

VIII. Expert Tips and Strategies for Smarter HELB Repayment in Kenya

To manage your loan efficiently, minimize interest, and ensure a smooth exit from the debt, incorporating these expert financial strategies is key.

A. Financial Planning and Budgeting Strategies

Proactive financial planning is the best defense against defaulting and incurring the heavy penalties associated with delayed HELB repayment in Kenya.

- Budgeting as a Statutory Deduction: Treat your HELB payment exactly like your taxes (PAYE) or NSSF contributions—it is a non-negotiable fixed cost. Incorporate it into your monthly budget the moment you secure your first salary.

- Overpayment Strategy: If financially feasible, pay slightly more than the minimum required amount each month. Even a small consistent overpayment can significantly reduce the principal balance faster, thus reducing the overall interest accrued over the life of the loan.

- Lump-Sum Payments: Dedicate bonus payments, tax refunds, or unexpected windfalls entirely to reducing your principal. HELB repayment in Kenya benefits immensely from large one-off payments as they directly cut the interest calculation base.

B. Leveraging Technology and Communication

The digital landscape offers tools that enhance control and transparency over your HELB repayment in Kenya process.

- Automate Payments: If you are self-employed like Host Kenya and Marsha Creatives or a gig worker, set up a standing order from your bank or a recurring payment alert on your phone. This automation ensures consistency and protects against forgetting the payment deadline.

- HELB Mobile App: Use the official app regularly to check your statement balance, verify recent payments, and ensure that all remittances (especially employer deductions) are accurately reflected.

- Stay Informed: Immediately update your contact information (phone number, email, and postal address) on the HELB portal. HELB uses these channels for critical updates, including penalty waivers or policy changes.

C. Navigating Hardship and Default Proactively

Never default silently. If you foresee or experience genuine financial hardship, communication is your most powerful tool for responsible HELB repayment in Kenya.

- Seek Deferment: If you lose your job or face a prolonged illness, immediately apply for the Jobless Moratorium or hardship deferment before the monthly penalty hits.

- Negotiate a Plan: If you are a chronic defaulter with massive arrears, visit a HELB service centre to formalize a repayment plan. Demonstrating willingness to pay is the single most important factor in securing a favorable negotiation and freezing the penalty accumulation.

- Record Keeping: Keep digital and physical copies of all official HELB communications, payment receipts, bank statements, and deferment approval letters. These records are vital if any dispute arises regarding your account status.

IX. Conclusion: Sustaining the Fund for Future Generations

The process of HELB repayment in Kenya in 2025 is defined by technological transparency, stricter compliance, and shared responsibility. By understanding the critical role the revolving fund plays and adhering to the clear, digital-first policies, you accomplish three key objectives:

- Financial Freedom: You successfully settle your debt, clear your name from the CRB, and secure the vital HELB Clearance Certificate.

- Legal Compliance: You avoid the heavy financial penalties, legal action, and guarantor liability associated with default.

- National Investment: You directly contribute capital back into the HELB fund, ensuring that future generations of Kenyan students have access to the same educational opportunities you did.

The future of Kenya’s higher education funding rests on the integrity and commitment of its beneficiaries. Start your compliant HELB repayment in Kenya journey today.

The journey of HELB repayment in Kenya is one of critical civic responsibility and personal financial discipline. This comprehensive guide has detailed the shifts in policy, the efficiency of digital platforms like eCitizen, and the necessity of proactive compliance in 2025. By adhering to the mandatory deduction schedules and leveraging the available penalty waivers, graduates not only secure their own financial future but also reinforce the educational foundation of the nation.

A. The Cumulative Power of Consistent Repayment

The concept of the revolving fund is simple, yet its impact is massive. Every timely installment, every successful remittance via the employer check-off system, directly translates into a loan being approved for a university or TVET student starting their academic journey.

- Data Impact: HELB manages billions of shillings annually, with a significant portion derived directly from recoveries. The higher the recovery rate, the less reliance on strained government budgetary allocations, making the fund robust and independent.

- The Ethical Angle: Settling your debt contributes to a culture of integrity and reciprocity, proving that the faith placed in students via the loan system is warranted.

B. Final Checklist for Seamless HELB Repayment in Kenya

To ensure you move smoothly from loanee status to a fully compliant graduate, keep this final checklist in mind:

| Action Item | Frequency | Rationale |

| Check Statement & Compliance | Monthly / Quarterly | Verify employer deduction remittance and track interest accrual. |

| Update Contact Details | Annually or upon change | Ensure you receive critical communication regarding waivers or policy changes. |

| Save Payment Proofs | Every Transaction | Maintain records for any potential future disputes, especially with the employer check-off. |

| Apply for Deferment | Immediately upon job loss | Crucial step to pause the Ksh 5,000 monthly penalty. |

C. The Future Outlook for HELB Repayment in Kenya

Looking beyond 2025, the trend is clear: full digitization and personalized service.

- Increased Integration: Expect greater seamlessness between HELB, KRA, NSSF, and other government databases to make tracking more efficient and reduce loopholes for non-compliance.

- Potential for IBR: The continued discussion and eventual implementation of an Income-Based Repayment (IBR) model will transform the system, shifting the emphasis from fixed debt servicing to sustainable, income-proportionate contributions. This will make HELB repayment in Kenya fairer for all graduates.

Ultimately, your commitment to clearing your loan is your final act of investing in Kenyan education. Take control of your debt today to secure your tomorrow.