I. Introduction: What Is CRB in Kenya?

CRB, or Credit Reference Bureau, is a term that is crucial for anyone who plans to borrow money or access financial services in Kenya. Simply put, CRB is an institution that collects and manages credit information about individuals and businesses. Its role is to ensure that lenders have access to accurate information to assess the risk associated with lending money.

In Kenya, CRBs have become integral players in the financial ecosystem, helping banks, microfinance institutions, and even mobile lenders make informed decisions about who they lend to.

When you apply for a loan, whether it’s from a bank, a microfinance institution, or even through a mobile loan service like M-Shwari, CRB in Kenya plays a significant role in determining your creditworthiness.

How CRB in Kenya Works

CRBs collect data from various financial institutions, including:

- Banks

- SACCOs (Savings and Credit Cooperative Societies)

- Mobile lending platforms (e.g., M-Shwari, KCB M-Pesa)

- Utility companies (e.g., electricity, water, and mobile phone bills)

Once the data is collected, CRBs compile it into credit reports. These reports give a detailed picture of a borrower’s financial behavior—such as how well they pay back loans and bills, the frequency of defaults, and whether they have a history of late payments.

In Kenya, the Banking Act and the Credit Reference Bureau regulations govern the operations of CRBs, making sure they work within a legal framework that protects both borrowers and lenders. By having access to this data, lenders are able to make better, more informed decisions about whether or not to approve a loan or credit application.

Why Does CRB in Kenya Matter for Young Kenyans?

The importance of CRB in Kenya extends far beyond just loans and credit approval. It affects young people in several ways:

1. Building Financial Reputation

Young Kenyans, especially those just starting their careers or businesses, need to understand the importance of building a good credit history early on. Having a positive credit report from a recognized CRB can unlock numerous financial opportunities.

- What is a Credit Score?

- A credit score is a numerical representation of your creditworthiness. It’s derived from your credit history and is used by lenders to assess the risk of lending money to you. In Kenya, CRBs generate these scores, which range from low to high. A higher score typically means you are more likely to be approved for loans with better terms.

By establishing a positive credit history early in life, young Kenyans can access financial services more easily when they need them in the future.

2. Access to Financial Products

For many young people, access to financial products like loans, credit cards, or mortgages is crucial for their personal and professional growth. CRB in Kenya determines whether you qualify for these products. Without a good credit history, it becomes challenging to secure a loan or credit card from banks or other lenders.

- Loan Approvals: If your credit report shows a history of making timely payments, it significantly increases your chances of securing a loan, be it for a car, a home, or even starting a business.

- Mobile Loans: With mobile lending platforms like M-Shwari and KCB M-Pesa gaining popularity, young Kenyans are increasingly relying on CRB data to access quick loans. These platforms use your credit score from CRBs to determine your eligibility for a loan.

3. Financial Independence and Business Opportunities

Young Kenyans who are starting businesses or want to pursue entrepreneurial ventures also benefit from a good CRB record. As an entrepreneur, your personal credit score can affect your ability to get business loans or funding to expand your enterprise.

- Small Business Loans: Whether you’re seeking a loan to buy equipment or expand your business operations, a good credit history will make it easier to secure the funds you need.

- Personal Loans for Career Growth: Young people may also seek personal loans to finance further education or certifications. A positive credit report can help them access these opportunities.

Case Study: How CRB Affects Access to Loans in Kenya

Meet John, a Young Entrepreneur from Nairobi:

John, a recent university graduate, has started a small tech company in Nairobi. He needs a loan to buy the latest software and equipment to grow his business. However, when he applies for a loan through his bank, he is told that his credit score is too low for the bank to approve his loan.

John’s low credit score stems from a couple of late payments on his mobile loans in the past. Even though he has a steady income and his business is doing well, the CRB in Kenya system flags his history, affecting his ability to access further credit.

This scenario is all too common for young Kenyans, emphasizing why it’s crucial to maintain a good credit history from an early age. A single missed payment or delayed loan can have lasting consequences on your credit score and ultimately affect your access to essential financial products.

II. Understanding CRB in Kenya

A. The Role of CRB in Kenya

CRB (Credit Reference Bureau) plays a crucial role in Kenya’s financial ecosystem. Its primary function is to collect and maintain accurate credit information about individuals and businesses like Host Kenya and Marsha Creatives. By doing so, CRBs help create a system of financial accountability, ensuring that both lenders and borrowers engage in a transparent and fair process.

Entities Involved in CRB in Kenya

Several entities interact with CRBs to ensure that the information in credit reports is accurate and up-to-date:

- Central Bank of Kenya (CBK): As the main regulatory body overseeing financial institutions in Kenya, the CBK regulates CRBs and ensures they follow the legal framework set out in the Banking Act and Credit Reference Bureau regulations.

- Licensed Credit Reference Bureaus (CRBs): These are institutions like TransUnion, Metropol, and CRB Africa, licensed by the Central Bank of Kenya to gather and store credit information. They work closely with financial institutions to provide up-to-date credit data

- Financial Institutions: Banks, SACCOs, microfinance institutions, and mobile lenders are the primary sources of data for CRBs. These institutions report customer credit activities to the CRBs, which includes loan repayments, defaults, and outstanding debts.

- Utility Companies: In Kenya, even utility companies such as Kenya Power (electricity) and Kenya Water contribute to credit information sharing. Mobile money services like Safaricom’s M-Pesa also play an important role, particularly with regard to mobile loans and bill payments.

What Does CRB in Kenya Do?

CRBs in Kenya serve multiple functions, all of which help maintain the financial system’s integrity:

- Collects Credit Information: CRBs gather data from banks, SACCOs, utility companies, and even mobile phone lenders. This data is compiled into a credit report for individuals and businesses.

- Maintains Credit Reports: These reports show a borrower’s history with various financial institutions, including details like how many loans they have taken, whether they paid them back on time, and if they defaulted on any payments.

- Creates Credit Scores: Based on the credit history, CRBs generate credit scores. These scores indicate an individual’s creditworthiness and determine their ability to access financial products.

- Enables Lenders to Make Informed Decisions: Banks and other lenders use the information in CRB reports to assess whether a person or business is a good risk. If someone has a high credit score (i.e., a history of responsible borrowing and repayment), they are more likely to be approved for a loan or credit card with favorable terms.

How CRB Reports Help Lenders in Kenya

The role of CRB reports in the Kenyan financial system cannot be overstated. When financial institutions evaluate a loan application, they use CRB data to assess the applicant’s creditworthiness. Here’s how it works:

- Credit Reports: These give a detailed account of an individual’s credit history, showing whether they’ve repaid loans on time, whether they’ve been flagged for defaulting, and how much debt they currently owe.

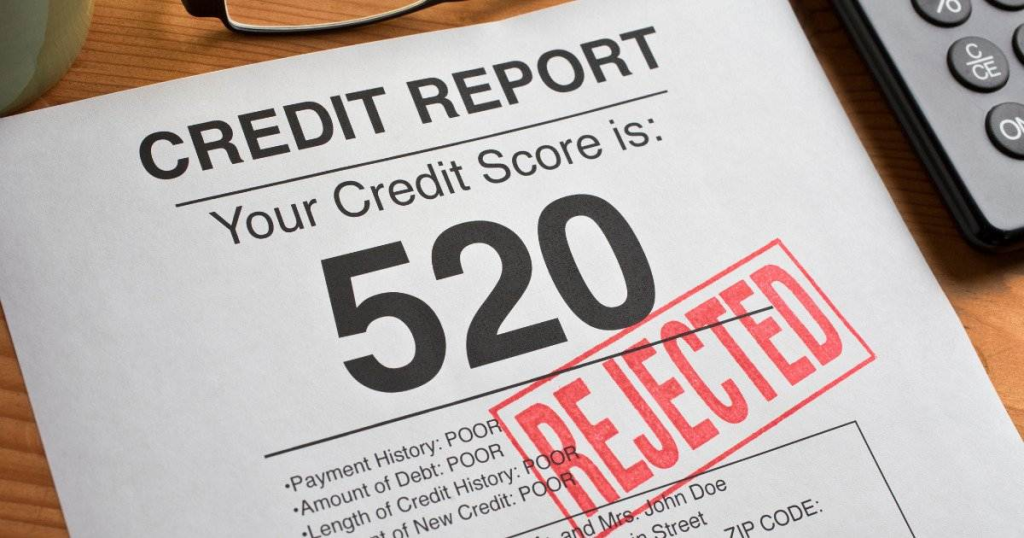

- Credit Scores: A credit score is derived from the data on your credit report. The score typically ranges from 300 to 850—a higher score indicates a good credit history. A low score can result in loan rejections or higher interest rates on loans.

- Risk Assessment: By using CRB reports and scores, lenders can determine the risk associated with lending money to an individual. If someone has a track record of making late payments or defaulting on loans, lenders may be less willing to approve their loan application.

B. How CRB Works in Kenya

CRB in Kenya operates within a structured system that allows financial institutions to share credit information and make informed lending decisions. Below is an in-depth look at how CRBs function in Kenya:

The Legal Framework Governing CRBs

CRBs in Kenya operate under the Banking Act and the Credit Reference Bureau regulations issued by the Central Bank of Kenya. These laws set guidelines for:

- Information Sharing: Financial institutions are required to share data with CRBs. This includes both positive data (like timely loan repayments) and negative data (such as defaults or missed payments).

- Consumer Protection: The regulations protect consumers by ensuring that they can access their credit reports and dispute any errors found in their credit history.

- Accuracy of Data: The law mandates that the data collected and shared by CRBs must be accurate and up-to-date. This ensures that consumers are not unfairly penalized due to inaccurate or outdated information.

How CRBs Collect Data

CRBs in Kenya gather data from a variety of sources:

- Banks and SACCOs: The primary sources of credit information, including loans, savings, and repayments.

- Mobile Loan Providers: With the rise of mobile-based financial services like M-Shwari, mobile lenders report credit data to CRBs as well. These lenders are becoming an increasingly important part of the Kenyan credit landscape.

- Utility Companies: Bills from utility services like Kenya Power or Safaricom can affect an individual’s credit score. Missed payments or defaults on utility bills may be recorded by CRBs.

- Microfinance Institutions and Other Lenders: Small lenders, including microfinance institutions, also report credit information to CRBs.

Once the data is collected, CRBs generate a credit report and credit score for individuals and businesses. This report includes:

- Personal Information: Name, ID number, contact details.

- Credit History: A detailed list of loans, their repayment status, defaults, and outstanding balances.

- Credit Inquiries: Records of when and why a lender accessed your credit report.

How CRBs Protect Consumers’ Rights

While CRBs play a crucial role in promoting transparency and reducing the risk of lending, they also have responsibilities toward consumers. Key protections for consumers include:

- Right to Access Credit Reports: Consumers have the right to request their credit report from CRBs at any time. This allows them to check for accuracy and understand their credit standing.

- Right to Dispute Errors: If a consumer notices any inaccuracies in their credit report, they can dispute the data with the CRB. The CRB must investigate and correct any errors.

- Time Limit for Negative Information: Negative credit information, such as defaults, can only stay on a credit report for a limited period (usually 7 years), after which it should be removed.

CRB and Financial Inclusion

In Kenya, CRB in Kenya plays a significant role in promoting financial inclusion. By maintaining transparent and accurate credit data, CRBs make it easier for unbanked individuals or those with no prior credit history to access financial products. CRBs help establish a formal credit history, which is particularly valuable for young people and small business owners who are trying to establish themselves in the financial system.

Key Takeaways:

- CRB in Kenya is essential for creating a transparent and responsible financial ecosystem.

- CRBs collect credit data from banks, SACCOs, mobile lenders, and utility companies to generate credit reports and scores.

- Lenders use this data to assess a borrower’s risk and make lending decisions.

- CRBs operate under a regulatory framework set by the Central Bank of Kenya, ensuring consumer protection and data accuracy.

- Access to CRB reports allows individuals to monitor their credit history and improve their creditworthiness.

III. What is a Credit Score and How Does It Work?

A. What Is a Credit Score?

A credit score is a crucial component of your financial health, particularly when it comes to accessing loans, credit cards, and even securing housing or certain jobs. In Kenya, a credit score is generated from your credit report, which reflects your history of borrowing and repaying money. CRBs in Kenya assign a score based on the information available in your report.

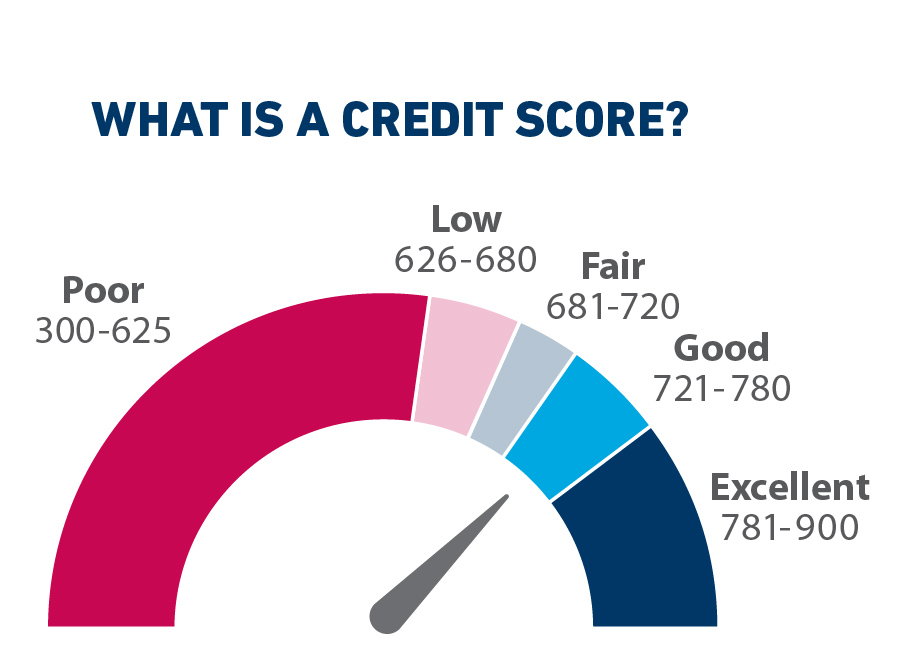

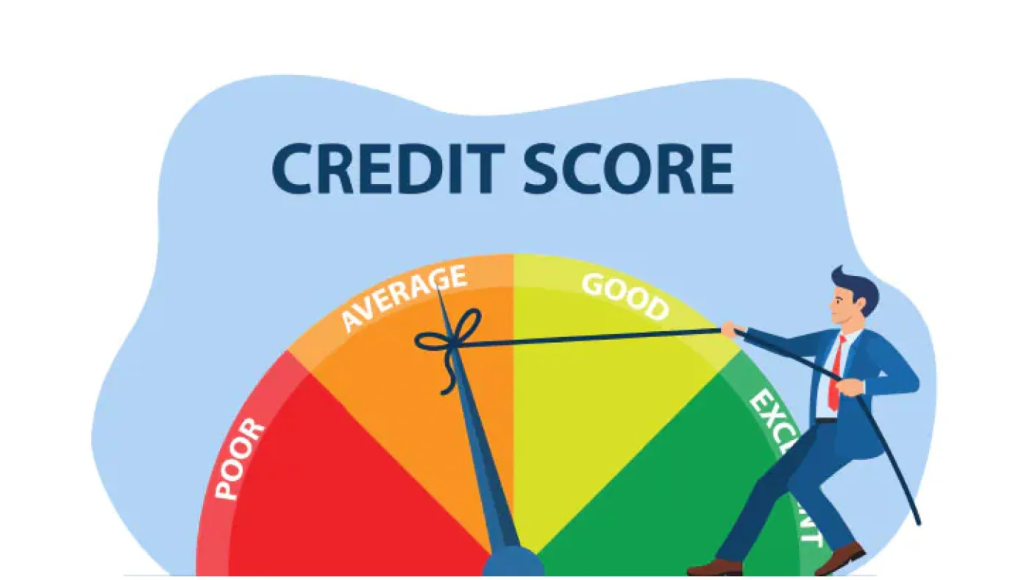

Understanding the Credit Score Scale in Kenya

Credit scores typically range from 300 to 850. Here’s a breakdown of how these scores are typically categorized:

- 300-500 (Poor): A score in this range suggests that the individual has a poor credit history, including missed payments, defaults, or high levels of outstanding debt. Such individuals will likely face difficulties when applying for loans, and if they do get approved, it’s usually at a high-interest rate.

- 500-650 (Fair): A fair score means that while the individual may have made some late payments in the past or has some debt, they have generally been responsible. Loan approval is still possible, but the terms may not be favorable.

- 650-750 (Good): This range indicates a solid credit history with a mix of loans paid on time, low credit utilization, and responsible borrowing. Lenders are more likely to approve loans, and the interest rates may be lower.

- 750-850 (Excellent): An excellent credit score signifies a strong history of responsible credit management. People in this range are likely to get the best loan terms, including low-interest rates and favorable repayment schedules.

B. Key Factors Affecting Your Credit Score

Your credit score isn’t arbitrary; it’s based on several key factors that are used to assess your creditworthiness. Here are the primary components that determine your score in CRB in Kenya systems:

1. Payment History (35%)

Your payment history is the most significant factor affecting your credit score. This includes:

- Timely payment of loans.

- Paying utility bills on time.

- Avoiding defaults or late payments.

When you make a payment after the due date, it negatively impacts your score. Defaulting on a loan or missing several payments can cause a substantial drop in your credit score.

2. Amounts Owed (30%)

This factor looks at how much debt you currently have and how much of your available credit you are using. This is also known as your credit utilization ratio.

- Credit Utilization: If you have a credit card with a limit of KSh 100,000 and you’ve spent KSh 50,000, your utilization is 50%. Generally, keeping your utilization below 30% is ideal for a positive credit score.

3. Length of Credit History (15%)

The length of your credit history affects your score. A longer credit history provides more data for CRBs to assess, giving them a better idea of how responsible you are with managing credit.

- Older Accounts: Accounts that have been open for many years are viewed positively by CRBs.

- New Accounts: Frequently opening new accounts may reduce your score, as it can signal financial instability.

4. Types of Credit Used (10%)

This looks at the variety of credit accounts you have. Having a healthy mix of credit cards, personal loans, mortgage loans, and other types of credit accounts can improve your score, showing lenders that you are capable of managing different forms of credit responsibly.

5. Recent Credit Inquiries (10%)

Each time you apply for a loan or credit, the lender conducts a hard inquiry to assess your credit report. While a single inquiry may not significantly affect your score, multiple inquiries over a short period can lower it. Too many recent credit inquiries may suggest you’re experiencing financial difficulties.

C. The Importance of a Good Credit Score in Kenya

Having a good credit score in Kenya can open the door to numerous financial opportunities, both for individuals and businesses. Here’s why it matters:

1. Access to Loans with Better Terms

With a high credit score, you are more likely to receive loan approvals from financial institutions. Not only that, but you will also be offered favorable loan terms, such as lower interest rates, longer repayment periods, and higher loan amounts.

For example:

- A young Kenyan looking to buy a car with a good credit score may get an interest rate of around 10-12%, while someone with a poor credit score might face rates of 20-25% or even be denied altogether.

2. Easier Access to Credit Cards

Credit cards are an important tool for young people starting their financial journeys. With a strong credit score, you can easily access a credit card with a reasonable credit limit. This can help you build a positive credit history if you manage it well.

3. Lower Insurance Premiums

Some insurance companies in Kenya may use your credit score as a factor in determining your premium rates. People with good credit scores are often offered lower premiums because they are considered to be less risky.

4. Renting Properties

When renting an apartment or house, landlords often check your credit history as part of the application process. A good credit score can help secure your rental agreement, especially for young people who may not have an established rental history.

D. How to Improve Your Credit Score in Kenya

If your credit score isn’t as high as you’d like, don’t worry. There are several steps you can take to improve it:

1. Pay Your Bills on Time

Timely payments are essential for improving your credit score. Whether it’s loan repayments, utility bills, or mobile loans, ensure that you always pay on time to avoid penalties and negative impacts on your score.

2. Reduce Your Debt

Work on paying off outstanding debts, especially high-interest loans. Aim to lower your credit utilization ratio by reducing the amounts owed on credit cards and loans.

3. Avoid Opening Too Many New Accounts

While it may be tempting to open several credit accounts to increase your borrowing potential, too many inquiries in a short period can lower your score. Only apply for credit when absolutely necessary.

4. Review Your Credit Report Regularly

You have the right to check your credit report for free in Kenya. Regularly reviewing it allows you to ensure that there are no errors or outdated information affecting your score.

Key Takeaways:

- A credit score is a vital component of your financial profile and can significantly impact your ability to access loans, credit cards, and even rent properties.

- A good credit score can result in lower interest rates and better financial opportunities, while a poor credit score may limit your access to financial services and increase costs.

- CRBs in Kenya calculate your credit score based on factors such as payment history, amounts owed, and the length of your credit history.

IV. Why CRB in Kenya Matters for Young Kenyans

A. Access to Financial Products

One of the primary reasons that CRB in Kenya is so important for young people is because it directly affects their ability to access various financial products. These include personal loans, credit cards, and mobile loans. For young Kenyans who are starting their careers or businesses, access to credit is often necessary for personal growth, career advancement, and entrepreneurship. Here’s how CRB affects access to these financial products:

1. Loans and Credit Cards

In Kenya, lenders rely heavily on credit reports to evaluate loan applications. A good credit score can help you secure a personal loan or a credit card with favorable terms. Conversely, a poor credit score can result in:

- Loan denials: If your credit history shows defaults, missed payments, or excessive debt, banks and SACCOs might reject your application.

- Higher interest rates: Even if you’re approved for a loan or credit card with a low credit score, you’re likely to face higher interest rates, which can make repayment more difficult in the long term.

2. Mobile Loans and Digital Credit

Mobile-based lending platforms like M-Shwari, KCB M-Pesa, and Branch have become extremely popular in Kenya, especially for young people. These platforms provide quick access to short-term loans through mobile phones, often with minimal paperwork and approval times.

However, these mobile lending services also rely on CRB in Kenya to assess your creditworthiness. Your credit score is used to determine:

- Whether you can access the loan.

- The amount you can borrow.

- The interest rate and repayment terms.

If your credit score is low, you may find it difficult to get loans from these platforms or could face higher interest rates.

B. Building Financial Reputation Early

For young Kenyans, building a financial reputation early on is one of the most significant reasons to pay attention to CRB in Kenya. Having a solid credit history can provide numerous benefits that set you up for long-term financial success.

1. The Importance of Starting Early

Young people who build their credit early on have more opportunities to access financial products throughout their lives. CRB in Kenya helps establish a record of your financial behavior over time. This record is crucial when you need:

- Car loans: If you plan to purchase a car, your credit history will be checked by lenders, and a positive credit history will increase your chances of securing a loan with reasonable interest rates.

- Mortgage loans: When you’re ready to purchase a house, a positive credit score can be a key factor in securing a mortgage loan with favorable repayment terms.

- Business financing: As you grow your career or start a business, your ability to access financing for capital investment or business expansion will depend significantly on your credit history.

2. The Power of Responsible Borrowing

A responsible borrower—someone who makes timely payments on loans, manages credit wisely, and avoids accumulating too much debt—can quickly build a strong credit report. For young people in Kenya, starting this process early offers them the chance to secure future loans and credit with favorable terms. Here are some tips for responsible borrowing:

- Always pay bills on time: Timely payments are one of the biggest factors in improving your credit score.

- Keep your credit utilization low: Avoid maxing out credit cards or taking out more loans than you can manage.

- Limit new credit applications: Too many inquiries can negatively impact your score, so apply for credit only when necessary.

C. Long-Term Financial Independence and Business Opportunities

A solid credit report from CRB in Kenya isn’t just about access to loans—it’s about building financial independence. By developing a good credit history early, young Kenyans can position themselves to make the most of long-term opportunities, such as:

- Investing in property: Many young people in Kenya dream of owning homes or commercial property. A good credit score makes it easier to get a mortgage, which is essential for achieving this goal.

- Starting a business: Aspiring entrepreneurs often need start-up capital to launch their businesses. A strong credit history can make it easier to secure business loans or angel investments.

- Personal development: As you build your financial history, you also create opportunities for self-improvement. With access to credit, young people can pursue education, career growth, and other personal goals that require financial investment.

Case Study: The Role of CRB in a Young Kenyan Entrepreneur’s Journey

Meet Jane, a 25-Year-Old Kenyan Entrepreneur:

Jane is a young entrepreneur who recently opened a small fashion boutique in Nairobi. To grow her business, she needs a loan to purchase stock and invest in marketing. However, Jane is struggling with getting approved for a business loan because of her poor credit score, which was affected by several late payments on past mobile loans.

If Jane had taken steps earlier to improve her credit score by paying bills on time and keeping her debt manageable, she would have been in a better position to access financing. This situation highlights the importance of maintaining a good credit score not only for personal loans but for entrepreneurial success as well.

Key Takeaways :

- CRB in Kenya significantly impacts your ability to access key financial products, including loans, credit cards, and mobile loans.

- Building a positive financial reputation early helps young Kenyans access credit in the future, whether for personal goals or business expansion.

- Maintaining a good credit history through responsible borrowing opens the doors to long-term financial independence and investment opportunities.

V. Common Myths About CRB in Kenya

A. “Only People with Loans Are Affected by CRB”

One of the biggest misconceptions about CRB in Kenya is that only individuals with formal loans or credit accounts are affected by their credit history. While it’s true that people who take loans or use credit cards are often more aware of their credit reports, even those who don’t actively use credit can still be affected by CRB in Kenya.

Why This Is a Myth

In Kenya, credit information is not limited to just loans from banks or SACCOs. Mobile loan platforms like M-Shwari and KCB M-Pesa also contribute data to CRBs. Furthermore, utility companies like Kenya Power and Safaricom report payment information related to electricity bills and mobile money loans. Even if you haven’t taken out a formal loan, missed or delayed payments on your utility bills or mobile loans can impact your credit score.

- Mobile Loans: If you use mobile loans and fail to repay them on time, the information will be reported to CRBs, which can affect your credit score.

- Utility Bills: Defaulting on utility bills or paying them late can also negatively impact your credit report. Therefore, even if you don’t use traditional credit products, CRB in Kenya still affects you.

B. “One Late Payment Will Ruin My Credit Forever”

Another common myth is that a single missed payment or late repayment will permanently damage your credit score. While a late payment can certainly have a negative impact on your credit history, it doesn’t mean you are doomed to a poor score forever.

Why This Is a Myth

In reality, CRBs in Kenya typically update credit reports regularly, and one late payment does not automatically mean your credit is ruined for life. Here’s why:

- Impact of Late Payments: The impact of a missed payment will depend on how recent the payment was, as well as how many other positive payments you’ve made. A single missed payment will cause a temporary drop in your score, but if you consistently make payments on time after that, your score can improve.

- Credit Recovery: It is possible to recover from missed payments over time. By managing your finances better, paying bills on time, and keeping credit utilization low, you can rebuild your credit score. Negative information typically only stays on your credit report for up to 7 years in Kenya, after which it is removed.

- Disputing Errors: If you believe a late payment is incorrect or the result of an error, you can dispute it with the CRB. If the information is found to be inaccurate, it will be corrected, and your score will improve.

C. “CRBs Only Focus on Negative Information”

Many people assume that CRBs in Kenya only report negative data, such as missed payments or defaults. However, this is not the case. Credit reports compiled by CRBs include both positive and negative information.

Why This Is a Myth

CRBs are responsible for collecting all relevant information that paints a complete picture of a borrower’s creditworthiness. This means your credit history includes:

- Positive Data: Timely payments, low credit utilization, and successful loan repayments are all included in your report, and they help improve your credit score.

- Negative Data: Missed payments, defaults, and excessive debt are also part of your credit report, and these can negatively affect your credit score.

The key takeaway is that good credit behavior can help you maintain or improve your credit score, and CRBs track both positive and negative financial activities.

D. “You Can’t Check Your Own Credit Report”

Many Kenyans are unaware that they are entitled to check their own credit report for free. A common myth is that CRBs in Kenya restrict access to personal credit reports, but this is far from true.

Why This Is a Myth

According to Kenyan law, individuals have the right to request their credit reports from CRBs, and they are entitled to one free report per year. This allows you to:

- Check for Errors: By reviewing your credit report, you can ensure that all the data is accurate. If there are any mistakes, such as incorrect information about missed payments, you can dispute them with the CRB to correct your report.

- Monitor Your Credit: Regularly checking your credit report helps you stay on top of your credit status, making it easier to take corrective actions if necessary.

- Improve Financial Literacy: By understanding how credit reports work and what factors influence your score, you can make better financial decisions moving forward.

E. “Only People with Bad Credit Need to Worry About CRBs”

Another misconception is that only those with bad credit need to worry about CRB in Kenya. In reality, everyone who uses credit—whether they have good or bad credit—needs to be aware of how CRBs affect their financial lives.

Why This Is a Myth

Your credit report and score are used by lenders, landlords, employers, and even some insurance companies to assess your financial responsibility. So even if you have a good credit score, it’s important to understand how the system works and how your credit behavior can influence your financial future.

A good credit score gives you better access to loans, credit cards, and lower interest rates. It can also help you when renting properties, securing insurance, or even when applying for certain jobs, particularly those in the financial sector.

Key Takeaways:

- CRB in Kenya doesn’t only track loans or traditional credit; it also includes mobile loans, utility bills, and more.

- Late payments don’t permanently ruin your credit score; with responsible financial management, you can recover and improve your score.

- CRBs track both positive and negative information, so it’s important to maintain good credit habits.

- You have the right to check your own credit report, which helps you stay informed and fix any errors.

- Everyone, whether they have good or bad credit, should pay attention to their CRB report and manage their financial behaviors carefully.

VI. How to Avoid Negative CRB Listing

A. Managing Debt and Loans Effectively

One of the most important ways to avoid negative listings on CRB in Kenya is to manage your debts and loans responsibly. A few simple strategies can help ensure that you don’t fall behind on payments or accumulate too much debt, both of which can negatively impact your credit score.

1. Create a Budget

Creating a budget is the first step in taking control of your finances. A good budget will help you track your expenses, manage your income, and ensure that you have enough funds to make timely payments on any debts or bills.

- Track Income and Expenses: Know exactly how much money is coming in and where it’s going. This will help you prioritize essential payments, such as rent, bills, and loan repayments.

- Emergency Fund: Aim to set aside a portion of your income for emergency savings. This fund can help cover unexpected expenses, preventing you from missing payments if something unforeseen happens.

2. Stick to Your Repayment Schedule

On-time payments are the key to maintaining a good credit score. If you consistently make your payments by the due date, you will avoid the risk of being listed negatively by CRBs. Here are some tips for ensuring timely payments:

- Set Up Automatic Payments: Many financial institutions allow you to set up automatic payments for your loans or bills. This ensures that you never miss a payment.

- Remind Yourself of Due Dates: Use calendar apps or reminders to ensure that you’re always aware of your payment deadlines.

3. Avoid Over-Borrowing

Borrowing more money than you can realistically pay back is a quick way to end up with a poor credit score. Before taking out a loan or using credit, make sure you can afford to repay it within the agreed-upon time.

- Loan Assessment: Before applying for a loan, take time to assess whether the loan amount and repayment terms are within your budget.

- Only Borrow What You Need: Avoid borrowing excessively, especially for non-essential items. Stick to what you can comfortably repay.

4. Communicate with Lenders

If you’re facing financial difficulties, don’t hesitate to communicate with your lender. Most financial institutions are willing to work with borrowers who are going through difficult times. You may be able to negotiate more flexible repayment terms or defer payments without negatively impacting your credit report.

B. Regularly Check Your Credit Report

It’s important to check your credit report regularly to stay informed about your CRB status. In Kenya, you’re entitled to request your credit report from licensed CRBs at no cost once a year. By checking your report frequently, you can:

1. Identify Issues Early

By monitoring your credit report regularly, you can spot any errors or discrepancies that might affect your credit score. For instance, if you notice a late payment listed that you never made, you can take action immediately to dispute it with the CRB.

2. Ensure Accuracy

It’s also important to ensure that your credit history is up-to-date. If you’ve repaid a loan or closed a credit account, make sure these changes are reflected in your credit report. If they aren’t, reach out to the CRB and ask them to update your information.

3. Dispute Inaccuracies

If you find an error on your report, such as a payment listed incorrectly or an account that should have been removed, you can dispute it. The CRB is required to investigate your dispute and, if necessary, correct the information. This process can help you prevent unnecessary negative listings from affecting your score.

C. Consider Alternative Credit Building Options

If you’re just starting out or you’re rebuilding your credit, there are several alternative ways to build credit without relying on traditional loans. These options can help you establish a positive credit history with CRB in Kenya:

1. Use a Credit Card Responsibly

One way to build your credit is by applying for a credit card. If you use it responsibly by paying off your balance in full every month, it can positively affect your credit score.

- Choose a Low-Limit Credit Card: As a beginner, opt for a low-limit credit card to avoid over-borrowing. Pay off the balance each month to build a solid credit history.

- Avoid Maxing Out Your Credit Card: A high credit utilization ratio can hurt your credit score. Try to keep your credit card balance below 30% of your credit limit.

2. Join a SACCO (Savings and Credit Cooperative Society)

In Kenya, SACCOs are a great alternative to traditional banks and can help young people build credit. When you borrow and repay loans through a SACCO, the information is shared with CRBs, helping you establish a positive credit history.

- Start with Small Loans: If you’re new to credit, begin by borrowing small amounts that you can easily repay. Over time, your credit score will improve, and you’ll be eligible for larger loans.

3. Use Mobile Loans to Build Credit

If you’re unable to access a traditional credit card or loan, mobile loans from platforms like M-Shwari or KCB M-Pesa can help you build credit. These platforms report your borrowing activity to CRBs, allowing you to establish a credit history.

- Pay Back On Time: Make sure you pay back any mobile loans on time to avoid being flagged negatively by CRBs.

- Start Small: If you’re new to mobile loans, start with small amounts to help build your credit before taking on larger sums.

Key Takeaways:

- Managing your debt responsibly and making timely payments are key strategies to avoid negative listings by CRB in Kenya.

- Regularly checking your credit report helps you spot errors early and ensure that your credit history remains accurate.

- If you’re starting or rebuilding your credit, consider alternative credit-building options such as credit cards, SACCOs, or mobile loans.

- Clear communication with lenders can help prevent missed payments from negatively affecting your credit score.

VII. The Future of CRB in Kenya

A. Financial Inclusion for Young People

One of the most important roles CRB in Kenya plays is in advancing financial inclusion for the youth. As Kenya becomes increasingly connected to the digital economy, there is a growing need for young people to have access to credit and financial services. CRBs have been pivotal in making financial systems more inclusive by allowing people without a traditional banking history to access credit.

1. Democratizing Credit Access

In Kenya, millions of young people, particularly those from low-income backgrounds, have historically been excluded from the formal financial system. However, CRB in Kenya is changing this by allowing data from mobile lenders, SACCOs, and even utility bills to be included in credit reports. This provides a credit history for individuals who might otherwise have no formal financial record.

- Mobile Lending Platforms: Services like M-Shwari, Branch, and KCB M-Pesa have made it possible for young Kenyans to access credit through their phones. These platforms use data from CRBs to assess creditworthiness, allowing individuals who may not have access to traditional loans to participate in the financial system.

- Empowering the Unbanked: With mobile money services like M-Pesa, millions of young Kenyans who have been excluded from formal banking can now build credit and access financial services. This inclusivity helps more young people create a financial profile, giving them the opportunity to secure loans for businesses, education, or personal needs.

2. Creating Opportunities for Small Businesses

Many young entrepreneurs in Kenya face challenges accessing capital to start or grow their businesses. CRB in Kenya offers an avenue for them to access business loans. By building a positive credit history, young business owners can show their creditworthiness and gain access to the funds they need to grow.

- Financing for Entrepreneurs: Financial institutions are increasingly turning to CRBs to assess whether to grant loans to small businesses. A solid credit score can make it easier for young entrepreneurs to access capital and scale their businesses.

- Improved Access to Investors: Investors and venture capitalists may also use CRB reports to assess the creditworthiness of business owners before deciding to invest. A positive credit history can increase a young entrepreneur’s chances of securing funding.

B. The Role of Technology in CRB and Credit Reporting

As technology continues to advance, CRB in Kenya is evolving with it. The rise of Fintech, mobile money, and blockchain technology is transforming the way credit data is collected, analyzed, and shared. Here’s how these innovations are shaping the future of CRB in Kenya:

1. Digital Credit Platforms and CRB Integration

The rapid growth of digital credit platforms is one of the most significant trends in Kenya’s financial sector. These platforms make it possible for individuals to access credit without the need for a physical bank. In many cases, these services use data from CRB in Kenya to assess credit risk and determine eligibility for loans.

- Instant Loan Approvals: With platforms like M-Shwari and Branch, borrowers can access loans within minutes of applying, and their creditworthiness is automatically assessed through data provided by CRBs. This level of automation makes it easier for young people to get credit without the lengthy approval process associated with traditional banks.

2. The Rise of Alternative Credit Scoring

As more data becomes available, alternative credit scoring models are being developed. These models rely on a wider range of data to assess creditworthiness, beyond traditional credit history. For example:

- Social Media and Payment History: Some new systems explore a borrower’s behavior on social media platforms or track payments made via mobile money services like M-Pesa. These alternative data points could be used in future CRB systems to generate more accurate and comprehensive credit reports for young people.

3. Blockchain and Secure Data Management

Blockchain technology could transform the way CRBs manage and store credit data. Blockchain’s decentralized nature provides an opportunity to create more secure, transparent, and accessible credit data systems. This could increase trust in CRB systems by ensuring that data is accurate, tamper-proof, and easily accessible for both lenders and consumers.

- Data Privacy and Security: Blockchain technology could also address concerns around data privacy, ensuring that personal financial data is securely stored and only accessible by authorized parties. This is particularly important as financial institutions continue to integrate CRBs into their decision-making processes.

C. Potential Reforms and Government Initiatives

The Kenyan government has taken steps to improve the CRB system and ensure that it benefits both consumers and lenders. However, there is still room for improvement in the regulatory environment. Here’s a look at what could be on the horizon for CRB in Kenya:

1. Financial Literacy Campaigns

To ensure that CRB in Kenya serves its intended purpose of improving access to credit, there needs to be an increased focus on financial literacy. Many young Kenyans are not fully aware of how their credit score works or how it impacts their ability to get loans.

- Government-Backed Financial Education: There could be more widespread government-led initiatives to educate young people on managing credit responsibly, understanding credit scores, and making informed financial decisions. Such education could empower young Kenyans to use the CRB system to their advantage.

2. Expanding Access to Credit for the Youth

There is also a growing call to make it easier for young people to access credit, even without a perfect credit history. Some reforms could include:

- More Accessible Microloans: Introducing more affordable and accessible microloans could provide young people with the opportunity to build their credit histories.

- Government Guarantees for Youth Loans: The government could step in to offer loan guarantees for young people who are just starting to build their credit history. This would reduce the risk for lenders, making them more willing to extend credit to first-time borrowers.

3. Improving Transparency and Regulation

While CRBs in Kenya have come a long way, more regulation could be put in place to ensure transparency and fairness in the credit reporting process. The following measures could help improve the CRB system:

- Clearer Dispute Resolution Processes: Ensuring that individuals can easily resolve disputes with CRBs if they believe inaccurate information is harming their credit score.

- Enhanced Privacy Protections: Strengthening data privacy laws to prevent unauthorized access to credit reports and ensuring that consumers have more control over their personal financial information.

Key Takeaways:

- CRB in Kenya is playing an essential role in advancing financial inclusion for young people, making it easier for them to access credit and financial products.

- Technological advancements like Fintech and blockchain are transforming the way credit data is managed and assessed, which will likely make the CRB system more efficient and accessible.

- Government initiatives aimed at increasing financial literacy and improving access to credit could further empower young people to take control of their financial future.

VIII. Conclusion: Why CRB in Kenya Matters for Your Financial Future

A. Recap of the Importance of CRB for Young Kenyans

As we’ve explored throughout this article, CRB in Kenya plays a pivotal role in shaping the financial landscape for young people. From helping individuals build a credit history to enabling access to financial products, CRB in Kenya serves as a bridge between young borrowers and lenders, ensuring that both parties are informed and financially responsible.

Key Points to Remember:

- Building a Good Credit History: Starting early and maintaining a positive credit history with CRB in Kenya can unlock numerous financial opportunities, including access to loans, credit cards, and even employment opportunities.

- Impact on Financial Opportunities: Your credit score can significantly influence your ability to get approved for loans, credit cards, and other financial products. A good credit score leads to better loan terms and lower interest rates.

- Financial Independence and Business Growth: For young entrepreneurs, CRB in Kenya is essential in securing loans for business growth. Building a positive credit report early on gives young business owners better access to funding.

- Mobile Lending Platforms: Services like M-Shwari, KCB M-Pesa, and other mobile loans are increasingly used by young people in Kenya, making it easier to access credit through CRBs.

B. Key Takeaways for Young Kenyans

The CRB in Kenya system is more than just a tool for assessing creditworthiness; it’s a vital part of your financial journey. Whether you’re starting your career, planning to buy a house, or launching a business, your credit report and credit score will be a key determinant in your financial success.

Steps You Can Take to Manage Your CRB Status:

- Build Your Credit Early: Start building your credit by making small, manageable loans or using a credit card responsibly. Make sure to pay on time to keep your credit score high.

- Regularly Check Your Credit Report: Make it a habit to check your credit report at least once a year. This will help you stay on top of your financial health and spot any errors early.

- Avoid Over-Borrowing: Be cautious about taking on too much debt. Stick to borrowing only what you need and ensure you can afford to repay it.

- Pay Your Bills on Time: Timely bill payments, including utility bills and mobile loans, can have a significant impact on your CRB report.

- Take Advantage of Alternative Credit: If you’re just starting, consider using SACCOs or mobile loans to build your credit history, as they are increasingly being reported to CRBs.

C. Final Tips for Aspiring Young Borrowers

The future of financial inclusion in Kenya is bright, and CRB in Kenya is at the heart of it. As young people become more financially literate and take steps to manage their credit, they will be better equipped to access the opportunities they need to succeed.

Here are some final tips to ensure you make the most of the CRB system:

- Focus on Long-Term Financial Health: Building and maintaining a good credit score takes time. Consistent, responsible financial behavior is the key to long-term success.

- Stay Informed: Financial products and CRB regulations continue to evolve. Stay up-to-date on changes to ensure you’re making informed decisions about your credit.

- Seek Help When Needed: If you’re ever unsure about managing your credit or need assistance with your credit report, consider speaking to a financial advisor or using credit counseling services.

D. Looking to the Future

The CRB system in Kenya is continuously evolving, especially as more data becomes available and technology plays a bigger role in financial services. The future holds exciting possibilities for young Kenyans as access to credit becomes easier and more inclusive. By managing your credit wisely today, you set yourself up for greater financial opportunities tomorrow.

Final Thoughts

CRB in Kenya is not just a tool for financial institutions—it’s a powerful tool for young people to take control of their financial future. By understanding how CRB in Kenya works and managing your credit carefully, you can access loans, build wealth, and achieve your personal and professional goals. Remember, your credit score is more than just a number; it’s a reflection of your financial responsibility and an important asset that can open doors to many opportunities.