I. Introduction

The vibrant pulse of Kenya’s economy is increasingly digital. From Nairobi’s bustling tech hubs to rural entrepreneurs leveraging smartphones, the way money moves is undergoing a profound transformation. In this evolving landscape, the role of online payment gateways in Kenya has become absolutely critical for any business, regardless of its size or sector. If you’re running an enterprise, a startup, or even a solo venture, understanding and implementing the right digital payment infrastructure is no longer a luxury—it’s a foundational element for success.

Why Online Payment Gateways are Crucial for Kenyan Businesses

Kenya has earned its reputation as a global leader in digital payment innovation, largely thanks to the groundbreaking success and widespread adoption of mobile money platforms like M-PESA. This unique financial ecosystem means that businesses must embrace digital payment solutions to effectively serve their customers and expand their reach.

Think of an online payment gateway as the secure bridge between your customer’s money and your business’s bank account. When a customer clicks “pay” on your website, the payment gateway springs into action. It encrypts their financial details, sends them securely to the relevant bank or mobile money provider for authorization, and then confirms whether the transaction was successful. This seamless, behind-the-scenes process is what enables everything from quick e-commerce purchases to recurring service payments.

The importance of integrating robust payment gateways in Kenya cannot be overstated. Here’s why they are crucial:

- Enhanced Customer Experience: In 2025, Kenyan consumers expect convenience. They want to pay quickly and securely using their preferred methods, whether it’s M-PESA, a credit card, or another mobile wallet. A smooth checkout process powered by a reliable gateway reduces cart abandonment and builds customer trust.

- Wider Market Reach: By accepting online payments, your business isn’t limited by geographical boundaries. You can sell to customers across Kenya and even internationally, tapping into new markets that were previously inaccessible. This is especially vital in an e-commerce market projected to reach US$922.10 million by 2025 in Kenya, according to Statista.

- Operational Efficiency: Automating payment collection through a gateway saves significant time and resources that would otherwise be spent on manual invoicing, cash handling, and reconciliation. This frees up your team to focus on core business activities.

- Improved Cash Flow: Many modern payment gateways in Kenya offer rapid settlement times, meaning funds from successful transactions reach your bank account quickly. This improves your business’s liquidity and financial health.

- Data and Analytics: Most gateways provide detailed dashboards and reports on transactions, sales trends, and customer behaviour. This invaluable data can inform your marketing strategies, product development, and overall business decisions.

- Security and Fraud Prevention: Online payments inherently carry risks. A reputable payment gateway invests heavily in security measures like encryption, tokenization, and fraud detection tools, protecting both your business and your customers from cyber threats and financial losses. With 91% of Kenyan SMEs already utilizing digital payment solutions and 70% investing in cybersecurity measures, security is a top priority for businesses operating online.

In essence, an effective online payment gateway is a powerful enabler of digital commerce. It transforms how your business interacts with its customers, streamlines operations, and sets the stage for sustainable growth in Kenya’s rapidly advancing digital economy. The country’s digital payments market is projected to grow at a Compound Annual Growth Rate (CAGR) of 14.1% between 2024 and 2028, reaching an estimated market value of US$14.54 billion by 2028, according to SDK.finance. This upward trend underscores the necessity of choosing the right payment partner.

What to Consider When Choosing a Payment Gateway in Kenya

Selecting the ideal payment gateway in Kenya is a crucial business decision that extends beyond simply comparing transaction fees. A strategic choice considers various factors, ensuring the solution aligns perfectly with your business model, customer preferences, and long-term growth aspirations. Ignoring these aspects can lead to increased costs, frustrated customers, and even security vulnerabilities.

Mobile Money Integration: The M-PESA Imperative

In Kenya, mobile money is not just a payment option; it’s a way of life. M-PESA, Safaricom’s mobile money service, boasts an astounding reach, with over 32 million active users as of recent reports, processing billions of dollars in transactions annually. For any business operating in Kenya, a robust M-PESA integration is absolutely non-negotiable.

Your chosen payment gateway must seamlessly support Lipa na M-PESA functionalities, specifically Pay Bill and Till Number options. These are the most common ways Kenyans pay for goods and services digitally. Without direct and frictionless M-PESA support, your business will effectively exclude a vast majority of the local consumer base. Look for gateways that offer:

- STK Push Integration: This is the preferred method, where customers receive a prompt on their phone to enter their M-PESA PIN, eliminating manual entry and reducing errors.

- Automatic Reconciliation: The gateway should automatically confirm payments and update order statuses, minimizing manual verification.

- Support for both Pay Bill and Till Numbers: Depending on your business model (e.g., Pay Bill for recurring payments or services, Till for retail/goods), ensure both are supported.

Case Study: Local Mama Mboga Goes Digital Consider a local fruit vendor in Nairobi who previously relied solely on cash. By integrating an M-PESA Till Number via a simple payment gateway, she can now accept digital payments. This not only offers convenience to her customers but also provides a digital record of sales, improving her financial tracking. Her daily sales volume increased by 15% within the first month of offering M-PESA payments.

Transaction Fees and Charges: Unpacking the Costs

While an obvious factor, dissecting the fee structure of payment gateways in Kenya requires careful attention. Fees can significantly impact your profit margins, especially as your transaction volume grows. Here’s what to look for:

- Setup Fees: Some older gateways might charge a one-time fee to activate your account. However, many modern providers now offer free setup to encourage adoption.

- Per-Transaction Fees: This is the most common charge, typically a percentage of the transaction value (e.g., 2.5% to 3.5%) or a flat fee (e.g., KES 30), or a combination of both.

- Example: If a gateway charges 3.0% + KES 10, a KES 1,000 transaction would incur KES 30 + KES 10 = KES 40. A KES 100 transaction would be KES 3 + KES 10 = KES 13. Understanding this breakdown helps you evaluate costs for both high and low-value transactions.

- Withdrawal/Payout Fees: Charges incurred when you transfer funds from your gateway account to your local bank account. These can be fixed or a small percentage.

- Currency Conversion Fees: If you accept international payments in foreign currencies, the gateway might charge a fee for converting those funds to Kenyan Shillings (KES).

- Monthly Maintenance Fees: Some gateways have a recurring monthly fee, regardless of your transaction volume.

- Chargeback Fees: These are penalties levied when a customer disputes a transaction and it is reversed. High chargeback fees can be damaging.

- Minimum Transaction Requirements: Some providers might have a minimum monthly transaction volume or value to avoid additional charges.

Tip: Always request a clear, itemized fee schedule from potential providers. Don’t be afraid to negotiate, especially if you anticipate high transaction volumes.

Supported Payment Methods: Offering Customer Choice

Beyond M-PESA, a truly versatile payment gateway in Kenya should cater to a diverse range of payment preferences. Offering multiple options enhances customer convenience and broadens your potential market. Key methods to consider include:

- Credit and Debit Cards: Support for major international cards like Visa, Mastercard, and American Express is essential for international customers and a growing segment of local cardholders.

- Other Mobile Money Services: While M-PESA dominates, supporting Airtel Money and Equitel Money can capture additional market segments.

- Bank Transfers/Direct Debits: Useful for larger transactions or B2B payments.

- International E-wallets: For businesses with global customers, integration with platforms like PayPal can be a significant advantage, as directly accepting PayPal in Kenya can be challenging for merchants.

Data Point: A study by Statista in 2024 revealed that while M-PESA accounted for over 70% of digital transactions in Kenya, credit/debit card usage for online purchases has seen a 12% year-on-year growth. This indicates a need for multi-channel support.

Settlement Duration and Accessibility: Your Cash Flow Matters

The speed at which funds from a successful transaction land in your bank account is called the settlement duration. For businesses, especially small and medium-sized enterprises (SMEs), cash flow is king.

- Real-time (T+0): Funds are available almost immediately. While rare for full bank settlements, some M-PESA integrations can approach this speed.

- Next-day (T+1): Funds settle within one business day. This is a highly desirable feature for good cash flow.

- Standard (T+2/T+3): Funds settle within two to three business days. This is common for card payments.

Faster settlements allow you to reinvest earnings sooner, manage inventory more effectively, and meet operational expenses without delay. For example, if you’re a fresh produce supplier who needs to pay farmers daily, a T+0 or T+1 settlement is crucial. The Central Bank of Kenya (CBK) has recently extended the operating hours for the Kenya Electronic Payment and Settlement System (KEPSS), the national Real Time Gross Settlement (RTGS) system, to 7 AM to 7 PM from July 1, 2025. This enhancement aims to improve the efficiency and accessibility of Kenya’s payments ecosystem, potentially leading to faster settlement times across the board.

Ease of Integration with E-commerce Platforms: Plug and Play Solutions

Your online payment gateway should be a seamless extension of your existing digital infrastructure. Clunky integration leads to technical headaches, delays, and potential errors. Look for providers that offer:

- Ready-made Plugins/Extensions: If your website is built on popular e-commerce platforms like WooCommerce (for WordPress), Shopify, Magento, or Prestashop, ensure the gateway has official, well-maintained plugins. This significantly simplifies setup and ongoing management.

- Comprehensive APIs (Application Programming Interfaces): For businesses with custom-built websites or mobile applications, a well-documented and robust API is essential. This allows your developers to integrate the payment functionality directly and securely.

- Sandbox Environment: A testing environment where your developers can try out integrations without affecting live transactions.

- Developer Support: Access to technical assistance, clear documentation, and online resources for any integration challenges.

Example: If you run a Shopify store in Kenya, choosing a payment gateway with a direct Shopify app or plugin (like Pesapal or Flutterwave) will save you weeks of development time compared to a gateway that only offers raw API integration.

Security Standards and Data Protection: Building Trust

In the digital realm, trust is earned through robust security. A data breach can be catastrophic for any business, leading to financial losses, reputational damage, and legal repercussions. Your chosen payment gateway in Kenya must prioritize and demonstrate adherence to the highest security standards.

Key security features and certifications to look for include:

- PCI-DSS Compliance: This is the Payment Card Industry Data Security Standard, a mandatory set of security requirements for any entity that stores, processes, or transmits credit card information. Ensure your gateway is PCI DSS Level 1 compliant, which is the highest level of certification. This protects both your business and your customers’ card data.

- SSL (Secure Sockets Layer) Encryption: Ensures that all data transmitted between your customer’s browser, your website, and the payment gateway is encrypted, preventing eavesdropping and tampering. Look for

https://in your website’s URL. - Fraud Prevention Tools: Advanced gateways employ sophisticated technologies to detect and prevent fraudulent transactions. These can include:

- 3D Secure (e.g., Verified by Visa, Mastercard SecureCode): Adds an extra layer of authentication for card-not-present transactions, requiring customers to verify their identity with their bank.

- Tokenization: Replaces sensitive card data with unique, non-sensitive “tokens,” reducing the risk if data is compromised.

- Address Verification System (AVS) & Card Verification Value (CVV): Checks cardholder details against bank records.

- Machine Learning Algorithms: Analyze transaction patterns to identify and flag suspicious activities in real-time.

- Data Protection Act (Kenya, 2019) Compliance: Ensure the gateway complies with local data privacy laws regarding the collection, processing, and storage of personal data.

Quote: “Security is not a product, but a process.” – Bruce Schneier. This sentiment is particularly true for payment processing. A good gateway offers continuous monitoring and updates to its security protocols.

Customer Support and Dispute Resolution: When Things Go Wrong

Even the most technologically advanced systems can encounter issues. When a customer’s payment fails or a dispute arises, efficient and responsive customer support from your payment gateway partner becomes invaluable.

Consider:

- Availability: Is support available 24/7, during business hours, or only via email?

- Channels: Do they offer phone, email, live chat, or a dedicated account manager?

- Response Time: How quickly do they typically respond to queries or urgent issues?

- Dispute Resolution Process: Understand their procedure for handling chargebacks and customer disputes. A clear and fair process can save your business time and money.

- Local Support: For Kenyan businesses, having local support teams who understand the unique market dynamics and payment nuances can be a significant advantage.

Choosing the right payment gateway in Kenya is a strategic investment in your business’s future. By carefully evaluating these factors, you can select a partner that not only facilitates transactions but also contributes to your growth, security, and customer satisfaction.

The 5 Best Online Payment Gateways in Kenya for Businesses

Navigating the multitude of online payment gateways in Kenya can be daunting. To simplify your decision, we’ve meticulously reviewed and selected the top five providers that consistently offer reliability, comprehensive features, and strong local relevance for Kenyan businesses. These gateways represent the gold standard for facilitating seamless transactions in the dynamic Kenyan digital economy.

1. M-PESA (Safaricom Daraja API)

Overview: It’s impossible to discuss payment gateways in Kenya without putting M-PESA at the forefront. Launched by Safaricom in 2007, M-PESA is not merely a mobile money service; it is the backbone of Kenya’s digital financial ecosystem. For businesses, direct integration with M-PESA is paramount, and this is primarily achieved through the Safaricom Daraja API. Daraja (“bridge” in Swahili) provides the technical framework for businesses to connect their systems directly to M-PESA, enabling various functionalities beyond simple Send Money.

Supported Methods: The Daraja API focuses on direct M-PESA functionalities, including:

- Customer to Business (C2B): This facilitates payments from a customer’s M-PESA wallet to your business’s Pay Bill or Till Number. This is crucial for e-commerce, utility payments, and service fees.

- Business to Customer (B2C): Allows your business to disburse payments to individual M-PESA users, ideal for salaries, refunds, or even marketing payouts.

- Business to Business (B2B): Enables payments between businesses with M-PESA business accounts.

- STK Push (Lipa na M-PESA Online): The most user-friendly method for customers to pay online, where a prompt appears on their phone to complete the transaction by entering their M-PESA PIN, eliminating manual entry of Till/Pay Bill numbers.

- Query Transaction Status: Allows you to verify the status of M-PESA transactions in real-time.

While M-PESA Global Pay exists for consumers to make international online card payments using their M-PESA wallet, businesses looking to receive diverse international card payments will typically integrate a broader payment gateway in Kenya like Flutterwave or DPO, which then settles to their local bank account or M-PESA.

Integration: The Daraja API is highly developer-centric. Safaricom provides extensive documentation, a sandbox environment for testing, and various API endpoints. For those less technically inclined, many third-party payment gateways in Kenya (like Pesapal or Flutterwave) already have robust Daraja integrations, allowing you to leverage M-PESA via their platforms without direct API coding. For direct integration, Safaricom requires a registered business, an active Pay Bill or Till Number, and a formal go-live request after successful sandbox testing.

Pros:

- Unrivaled Market Penetration and Trust: M-PESA’s ubiquity means virtually every Kenyan consumer is a potential customer. It’s a trusted and familiar payment method, leading to higher conversion rates for local transactions.

- Real-time or Near Real-time Settlement: Funds from C2B payments often reflect in your M-PESA business account almost immediately (T+0), or are quickly available for withdrawal to your bank (T+1), significantly boosting cash flow.

- Reduced Transaction Abandonment: The STK Push functionality simplifies the payment process, reducing errors and increasing successful transactions.

- Direct Access: No third-party fees beyond Safaricom’s standard M-PESA charges for business services.

Cons:

- Technical Integration Requires Expertise: Directly implementing the Daraja API needs a development team or technical partner.

- Limited International Card Processing: While versatile for local mobile money, it doesn’t inherently offer direct processing for international credit/debit cards on the merchant side.

- Safaricom’s Business Rules: Adhering to Safaricom’s specific operational and compliance guidelines is necessary.

Ideal for: Any business targeting the Kenyan domestic market. This includes e-commerce sites, digital service providers, utility companies, educational institutions, NGOs, and traditional brick-and-mortar businesses looking to offer cashless options. Its sheer market dominance makes it indispensable.

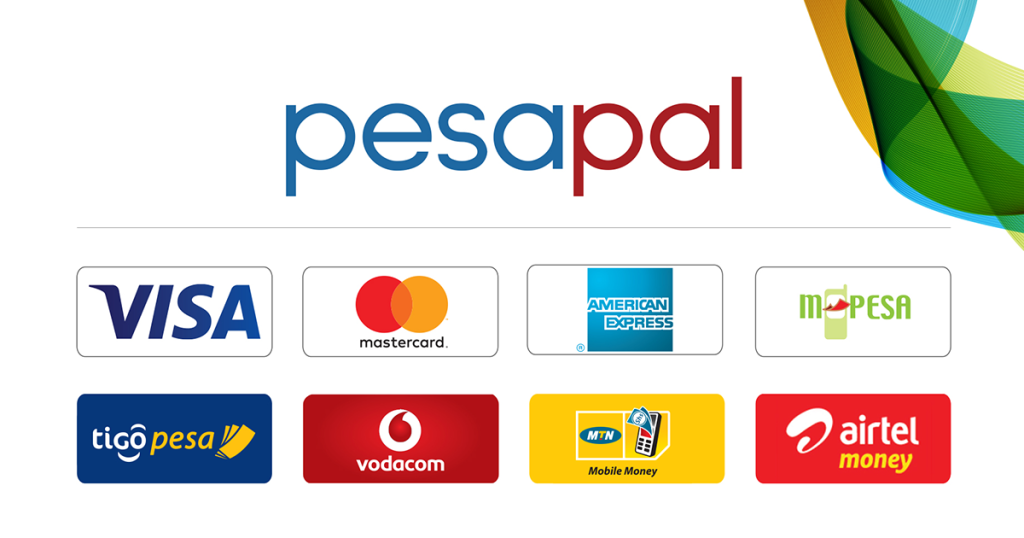

2. Pesapal

Overview: Pesapal is a homegrown Kenyan success story, established in 2009. It has grown to become one of East Africa’s leading payment gateways, offering a comprehensive suite of solutions designed to cater to the diverse payment needs of businesses in the region. Pesapal prides itself on being a one-stop shop, simplifying the complexities of accepting various local and international payment methods.

Supported Methods: Pesapal offers a strong blend of local and international payment options, making it highly versatile:

- Mobile Money: Excellent integration with M-PESA and Airtel Money, crucial for the Kenyan market.

- Credit/Debit Cards: Supports major cards including Visa, Mastercard, and American Express.

- Bank Transfers: Facilitates direct bank transfers.

This broad support means a business can use Pesapal to cater to both domestic customers who prefer mobile money and international clients or those who prefer card payments.

Integration: Pesapal excels in providing multiple integration pathways:

- E-commerce Plugins: Ready-made plugins for popular platforms like WooCommerce (WordPress), Shopify, Magento, and Prestashop ensure quick and easy setup for online stores.

- Comprehensive APIs: For developers creating custom websites or mobile applications, Pesapal offers a robust REST API and SDKs for various programming languages (e.g., PHP, Java, Python, .NET), along with thorough documentation.

- Hosted Payment Page: A simple, secure page hosted by Pesapal where customers are redirected to complete payment, minimizing your PCI compliance burden.

- Payment Links: Generate simple links to send via email or SMS for one-off payments without a full website integration.

Pros:

- Extensive Payment Options: A wide range of supported methods means you can cater to almost any customer.

- Strong Local Understanding & Support: Being a homegrown solution, Pesapal deeply understands the nuances of the Kenyan market and offers dedicated local customer support.

- User-Friendly Merchant Dashboard: Provides clear insights into transactions, settlements, and reporting, making financial reconciliation simpler.

- Robust Security: PCI DSS certified with advanced fraud monitoring tools to protect against illicit activities.

- Reliable Settlements: Funds typically settle within T+1 to T+3 business days to your local bank account.

Cons:

- Transaction Fees: While competitive, their percentage-based transaction fees can add up for high-volume, low-value transactions. For instance, card transaction fees typically range around 3.5%, while M-PESA fees can be lower. Always confirm the exact rates based on your business type and volume.

- Occasional Payout Delays: While generally reliable, some merchants have reported occasional delays in payouts, especially during public holidays or banking system updates.

Ideal for: Small to medium-sized e-commerce businesses, online service providers, educational institutions, and hospitality businesses that require a balanced approach to accepting both mobile money and card payments, with a preference for local support and ease of integration. Pesapal’s versatility makes it a strong contender for the majority of Kenyan online businesses.

3. Flutterwave

Overview: Flutterwave has rapidly emerged as a leading payment technology company across Africa, known for its innovative approach to simplifying complex payment infrastructures. Founded in 2016, it has quickly established a strong foothold in Kenya, offering a modern, developer-friendly platform that enables businesses to accept payments from customers worldwide and across the continent.

Supported Methods: Flutterwave offers one of the most comprehensive arrays of payment methods among payment gateways in Kenya, making it incredibly flexible for businesses with diverse customer bases:

- Major Credit/Debit Cards: Supports Visa, Mastercard, Verve, and American Express.

- Mobile Money: Robust integration with M-PESA in Kenya, alongside other mobile money options across different African countries (e.g., MTN Mobile Money, Vodafone Cash).

- Bank Transfers: Facilitates direct bank transfers.

- USSD: Allows payments via USSD codes, catering to feature phone users.

- International E-wallets including PayPal: This is a significant differentiator. Flutterwave enables businesses in Kenya to accept payments from PayPal users globally, bridging a crucial gap for international transactions that many local businesses struggle with.

Integration: Flutterwave is celebrated for its developer-friendly approach and ease of integration:

- Ready-made Plugins: Seamless integration with popular e-commerce platforms such as Shopify, WooCommerce, Magento, and PrestaShop.

- Robust APIs and SDKs: Comprehensive and well-documented APIs for various programming languages (Python, PHP, Node.js, Ruby, Java, .NET) and mobile SDKs (Android, iOS) make custom integration straightforward for developers.

- Payment Links: Quickly generate and share payment links for one-off invoices or social media sales.

- In-person Payments: Offers POS solutions for physical locations.

- Virtual Accounts: Provides virtual accounts to manage multi-currency transactions.

Pros:

- True Pan-African Reach: Ideal for businesses with regional expansion plans across multiple African countries, offering a unified payment experience.

- Critical PayPal Integration: A major advantage for businesses dealing with international clients, simplifying cross-border payments.

- Scalability: Designed to handle high volumes, making it suitable for businesses of all sizes, from startups to large corporations.

- Competitive Fees: Often offers competitive transaction fees, typically around 2.9% for local card payments and lower for mobile money, though international card fees can be higher (e.g., 3.8%). Confirm specific rates for Kenya as they can vary.

- Modern Platform and User Experience: Clean interface, intuitive dashboard, and real-time analytics.

- Fast Settlements: Generally, funds settle to your bank account within 1-5 business days (T+1 to T+5), depending on the currency and bank.

Cons:

- Occasional Service Interruptions: While reliable, like any large technology platform, there can be rare instances of temporary service disruptions.

- Initial Verification: The onboarding and verification process can sometimes be thorough, requiring comprehensive business documentation, which might take a few days.

Ideal for: E-commerce businesses with both local and international customer bases, SaaS companies, digital service providers, educational institutions attracting global students, and any business looking for a versatile, scalable, and globally connected online payment solution that can seamlessly handle both African and international transactions, particularly with PayPal.

4. Paystack

Overview: Acquired by Stripe in 2020, Paystack originated in Nigeria and has successfully expanded its footprint into Kenya, bringing its reputation for a developer-first approach and user-friendly payment solutions. Paystack aims to simplify online payments for businesses, focusing on reliability, speed, and ease of use.

Supported Methods: Paystack offers a range of payment options tailored for the African market:

- Credit/Debit Cards: Supports major international cards including Visa, Mastercard, and American Express.

- Bank Transfers: Allows customers to pay directly from their bank accounts.

- USSD: For mobile payments using feature phones.

- Mobile Money (M-PESA in Kenya): Paystack has been actively integrating and enhancing its M-PESA support in Kenya. While it was initially in beta, it is continuously improving to offer a seamless M-PESA experience for businesses. Current indications suggest strong M-PESA integration, offering competitive rates.

Integration: Paystack shines with its developer-centric design:

- Excellent API Documentation: Provides clean, well-structured, and extensive API documentation, making it a favourite among developers for custom integrations.

- SDKs: Available for various programming languages (Python, Node.js, PHP, Ruby, .NET, Go, etc.) and mobile platforms (Android, iOS, React Native, Flutter).

- Ready-made Plugins: Integrates smoothly with popular e-commerce platforms like Shopify, WooCommerce, Magento, and OpenCart.

- Payment Links & Invoices: Easily generate and send payment links or professional invoices for quick payment collection.

- Subscriptions & Recurring Payments: Robust tools for managing recurring billing.

Pros:

- Fast Onboarding: Businesses can often get their accounts approved and start accepting payments relatively quickly.

- Superior User Experience: Both the merchant dashboard and the customer checkout flow are intuitive, modern, and designed for simplicity, leading to higher conversion rates.

- Developer-Friendly: Highly praised for its comprehensive APIs, sandbox environment, and excellent developer support.

- Real-time Analytics: Provides detailed insights into transactions, customer data, and sales performance.

- Competitive Local Fees: Offers very competitive rates, with local card transactions typically around 1.95% (capped at KES 2,000 for high values) and M-PESA payments as low as 1.5%. International cards are around 3.2%.

- Fast Settlements: Funds are generally settled to your local bank account on the next business day (T+1), which is excellent for cash flow.

Cons:

- Evolving M-PESA Integration: While significantly improved, its M-PESA coverage might not be as deeply ingrained or have the sheer number of local-specific features as Pesapal, though it is rapidly catching up.

- Less Local Support Infrastructure (compared to Pesapal): As a relatively newer entrant in the Kenyan market compared to Pesapal, its local physical presence or depth of local support might still be developing.

Ideal for: Tech startups, SaaS companies, developers, and e-commerce businesses that prioritize a clean, modern interface, excellent developer tools, fast onboarding, and competitive fees. Its strong focus on user experience makes it ideal for businesses aiming to provide a seamless payment journey for their customers.

5. DPO Group (Direct Pay Online)

Overview: DPO Group, now part of Network International, stands as a formidable player among payment gateways in Kenya and across Africa. Established in 2007, it has built a strong reputation, particularly within the travel, tourism, and hospitality sectors. DPO offers a comprehensive and secure platform designed to handle high volumes of diverse transactions, positioning itself as a reliable partner for businesses with complex payment needs.

Supported Methods: DPO Group offers a vast array of payment methods, catering to both local and international customers:

- Mobile Money: Extensive support for M-PESA, Airtel Money, and other mobile money providers across its operational countries.

- Credit/Debit Cards: Comprehensive support for major cards including Visa, Mastercard, American Express, and Discover.

- Bank Transfers: Facilitates direct bank transfers.

- International Payment Options: Supports various international payment methods and multiple currencies, crucial for businesses with a global clientele.

Integration: DPO Group provides flexible integration options suitable for various business sizes and technical capabilities:

- E-commerce Plugins: Ready-made plugins for popular platforms like WooCommerce, Shopify, Magento, and many others.

- Comprehensive APIs: Robust APIs for custom web and mobile application development, with detailed documentation.

- Hosted Payment Page: A secure, customizable payment page hosted by DPO, simplifying PCI compliance for merchants.

- Virtual Terminal: Allows businesses to accept card payments over the phone or in person without a physical POS device.

- Specialized Solutions: Offers tailored solutions for specific industries like airlines, hotels, and tour operators, including features like fraud prevention tools specific to these sectors.

Pros:

- Strong Industry Expertise: Particularly well-regarded in the travel and hospitality sectors, with solutions designed to meet the unique demands of these industries (e.g., pre-authorizations, multi-currency pricing).

- Robust Fraud Prevention: DPO invests heavily in advanced fraud detection and prevention systems, offering a high level of security for both businesses and customers. This is crucial for high-value transactions common in tourism.

- Multi-Currency Support: Essential for businesses dealing with international clients, allowing them to accept and settle payments in various major global currencies.

- Pan-African and Global Reach: With a broad operational footprint, it’s ideal for businesses with cross-border operations or ambitions.

- Dedicated Account Management: Larger merchants often benefit from dedicated account managers and personalized support.

- Flexible Settlement Options: DPO offers various settlement methods, including direct bank transfers and even prepaid cards for faster access to funds (e.g., Payoneer Mastercard for same-day settlements in some cases), though standard bank settlements are typically T+1 to T+3 business days.

Cons:

- Potentially Higher Fees: While rates are competitive for high-volume enterprises, some smaller merchants might find their transaction fees slightly higher compared to some competitors, particularly for low-value transactions. Transaction fees can vary significantly based on volume and payment method, so direct consultation is advised.

- More Involved Onboarding: Due to their enterprise focus and stringent security requirements, the onboarding and verification process can be more detailed and potentially take longer than simpler gateways.

- Complexity: The sheer breadth of features might be overwhelming for very small businesses with basic needs.

Ideal for: Hotels, airlines, tour operators, large e-commerce platforms, and other businesses that process high volumes of transactions, deal with a significant international clientele, and require sophisticated fraud prevention and multi-currency capabilities. DPO’s comprehensive approach makes it a powerful partner for established and growing enterprises.

Side-by-Side Comparison: Which Payment Gateway is Right for Your Business?

Choosing the ideal payment gateway in Kenya boils down to understanding your business’s unique needs and comparing how each provider addresses those requirements. While all five listed are top-tier, their strengths often lie in different areas. This side-by-side comparison aims to highlight their key differences, helping you pinpoint the best fit.

Here’s a concise comparison table outlining the core features of the top online payment gateways in Kenya:

| Feature/Gateway | M-PESA (Daraja API) | Pesapal | Flutterwave | Paystack | DPO Group |

|---|---|---|---|---|---|

| Primary Focus | Mobile Money (Ksh) | Local & Int. Cards/MM | Pan-African Cards/MM/BT/PayPal | Cards/MM (evolving) | Pan-African, Travel/Hospitality |

| Key Supported Methods (Kenya) | M-PESA (Pay Bill/Till) | M-PESA, Airtel Money, Cards | M-PESA, Cards, Bank Transfers, PayPal | Cards, M-PESA (strong) | M-PESA, Cards, Bank Transfers |

| Integration Ease | Moderate (API) | Easy (Plugins/API) | Easy (Plugins/API) | Easy (Plugins/API) | Moderate (Plugins/API) |

| Local Card Fees (approx.) | N/A (mobile money) | ~3.5% | ~2.9% | ~2.9% (capped KES 2,000) | Varies, typically 2.5-3.5% |

| M-PESA Fees (approx.) | Safaricom rates | ~2.5% – 3.0% (variable) | ~2.9% | ~1.5% | Varies, typically 2.5-3.0% |

| International Card Fees (approx.) | N/A (consumer only) | ~4.0% | ~4.8% | ~3.8% | Varies, typically 3.5-4.5% |

| Settlement Time (to KES bank) | T+0/T+1 | T+1 to T+3 | T+1 to T+5 | T+1 | T+1 to T+3 |

| Customer Support | Via Safaricom | Responsive Local | Generally Good | Good, Developer-focused | Good, Enterprise-focused |

| Fraud Protection | Standard M-PESA | Good | Robust | Robust | Very Strong |

| PayPal Integration | No | No | Yes (for receiving) | No | No |

Export to Sheets

Note: All fees are approximate and can vary based on your business type, transaction volume, negotiation, and specific agreements with the payment gateway. It’s crucial to consult with each provider for their most current and tailored fee structures.

Recommendations by Business Type: Tailoring Your Choice

Understanding the nuances of each payment gateway in Kenya allows for a more targeted recommendation based on specific business needs:

- Small E-commerce Stores & Online Retailers (High volume of local transactions):

- Pesapal: A strong contender due to its excellent M-PESA integration and comprehensive support for other local and international card payments. Its user-friendly plugins for major e-commerce platforms like WooCommerce and Shopify make setup quick and relatively painless. The local support is also a significant advantage.

- Paystack: Increasingly competitive, especially with its very attractive 1.5% M-PESA fee and fast T+1 settlements. If your e-commerce platform integrates well with Paystack and you value quick access to funds, it’s an excellent choice for a predominantly local customer base.

- Insight: For businesses focused purely on the local Kenyan market, prioritizing a gateway with seamless M-PESA and competitive local fees is key.

- Freelancers & Consultants (Requiring easy invoicing and diverse client payments):

- Paystack: Its “Payment Links” feature is incredibly convenient. You can generate a link for an invoice and send it directly to your client via email, WhatsApp, or SMS. Its support for both cards and M-PESA, combined with fast settlements, is ideal for managing cash flow for services.

- Pesapal: Also offers payment links and a reliable platform for various payment methods. It’s a solid alternative if you prefer a locally established provider.

- Insight: For service-based businesses, simplicity of invoicing and diverse payment options for clients (both local and international) are paramount e.g Host Kenya and Marsha Creatives

- Hospitality & Tourism Businesses (Hotels, Tour Operators, Airlines – handling high-value international transactions):

- DPO Group: This is where DPO truly shines. Their specialized solutions for the travel industry, robust fraud prevention (critical for high-value transactions from international cards), and extensive multi-currency support are unmatched. They are designed to handle complex booking systems and secure large payments.

- Flutterwave: A strong alternative, especially if you also need to easily accept PayPal payments from international guests. Its pan-African reach can also be beneficial if you have regional operations or partners.

- Insight: These industries demand sophisticated fraud prevention, multi-currency capabilities, and often bespoke integrations with booking engines.

- Tech Startups & Developers (Building custom solutions, focusing on API-first approach):

- Safaricom Daraja API: If your core business model revolves heavily around M-PESA and you have the technical expertise to build custom integrations, going direct with Daraja offers maximum control and potentially lower long-term transaction costs.

- Paystack: Highly favored by developers for its clean, comprehensive, and well-documented APIs and SDKs. Its sandbox environment allows for seamless testing, accelerating development cycles.

- Flutterwave: Another strong contender for developers, offering robust APIs and SDKs across multiple languages, suitable for complex and scalable applications.

- Insight: For tech-driven businesses, the quality of API documentation, developer support, and flexibility for custom solutions are paramount.

- Businesses Expanding Across Africa (Requiring unified payment solutions across borders):

- Flutterwave: This is its strongest selling point. Flutterwave’s pan-African network allows businesses to accept payments from customers in multiple African countries through a single integration and dashboard, simplifying regional expansion and reconciliation.

- DPO Group: With a significant presence in over 20 African countries, DPO also offers extensive cross-border capabilities, particularly for larger enterprises.

- Insight: A unified regional payment solution drastically simplifies management and scalability for businesses with pan-African ambitions.

By carefully evaluating these recommendations against your specific business context, you can make a well-informed decision on the best payment gateway in Kenya to power your operations and fuel your growth in 2025 and beyond.

FAQs: Common Questions About Online Payment Gateways in Kenya

Navigating the world of online payment gateways in Kenya often brings up a host of questions, particularly for businesses new to digital commerce or those looking to optimize their existing setups. Here, we address some of the most frequently asked questions, providing clarity and practical insights for 2025.

What’s the cheapest payment gateway in Kenya?

Identifying the absolute “cheapest” payment gateway in Kenya isn’t a straightforward answer, as it heavily depends on several factors specific to your business:

- Transaction Volume and Value: Gateways often have tiered pricing. A gateway that’s cheap for high-volume, low-value transactions might be expensive for low-volume, high-value ones, and vice-versa.

- Payment Methods Accepted: Fees vary significantly between M-PESA, local card payments, and international card payments.

- Overall Cost Structure: Beyond per-transaction fees, consider setup fees, withdrawal fees, monthly maintenance fees, and potential hidden charges.

General Observations for 2025:

- Direct M-PESA (Safaricom Daraja API): For purely M-PESA transactions, going direct with Safaricom’s Daraja API and using their official business tariffs (Lipa na M-PESA Pay Bill/Till Number rates) can be very cost-effective. These rates are determined by Safaricom based on transaction value and can be quite competitive, especially for smaller amounts.

- Paystack: For local card and M-PESA payments, Paystack often stands out with its competitive rates. As of current information, their M-PESA fee is notably low at around 1.5%, and local card fees are typically 1.95% (capped at KES 2,000 for higher values). This makes them a strong contender for cost-efficiency, particularly for growing businesses.

- Pesapal & Flutterwave: While slightly higher than Paystack for local M-PESA (around 2.5%-3.0%), they offer strong overall value due to their comprehensive feature sets, ease of integration, and support for a wider range of payment methods.

Recommendation: The best approach to finding the cheapest payment gateway in Kenya for your business is to:

- Project Your Transaction Volume and Average Value: Estimate how many transactions you expect and their typical amounts.

- Identify Your Primary Payment Methods: Will most payments be M-PESA, local cards, or international cards?

- Request Detailed Quotes: Contact 2-3 preferred gateways and ask for a full breakdown of all potential fees based on your projected usage.

- Calculate Total Cost: Compare the total estimated cost, not just the per-transaction percentage.

Can I accept international payments through M-PESA directly?

This is a nuanced question with a practical answer:

- For Kenyan Consumers: Yes, Kenyan M-PESA users can make international online payments using services like “M-PESA Global Pay.” This typically links their M-PESA account to a virtual Visa card, allowing them to pay on international websites that accept Visa.

- For Kenyan Merchants (Receiving Payments Directly to M-PESA): Directly receiving international credit card payments into your M-PESA business till/pay bill is generally not how international payments are processed for merchants. Instead, online payment gateways in Kenya like Flutterwave and DPO Group act as intermediaries. They allow you to accept payments from international credit cards (Visa, Mastercard, etc.), PayPal, or other global payment methods. These funds are then settled to your local Kenyan bank account, or in some cases, converted and transferred to your M-PESA business account, depending on the gateway’s specific payout options.

M-PESA Global Merchants Program: Safaricom does have an “M-PESA Global Merchants” program which aims to simplify accepting payments from global M-PESA customers. This initiative is designed to enable international businesses to accept M-PESA payments. For Kenyan merchants looking to expand globally, this might enable receiving payments from M-PESA users in other countries where M-PESA operates (e.g., Tanzania, Rwanda, etc.) directly. However, for non-M-PESA international payments (e.g., a customer in the US paying with their American credit card), you’ll still need a comprehensive gateway like Flutterwave or DPO.

Do I need a business registration to use a payment gateway in Kenya?

Yes, for the vast majority of legitimate business operations, you will need a formal business registration to use a reputable payment gateway in Kenya. This is a critical requirement driven by:

- Know Your Customer (KYC) Regulations: Financial institutions and payment service providers are legally obligated to verify the identity of their clients to prevent money laundering, terrorism financing, and other illicit activities.

- Anti-Money Laundering (AML) Compliance: Strict global and local AML laws require payment gateways to have clear records of who they are processing money for.

- Tax Compliance: Businesses are expected to be tax compliant, and your registration details help the Kenya Revenue Authority (KRA) track taxable income.

Typical Business Registration Documents Required (as of 2025):

- Business Name Registration Certificate or Certificate of Incorporation (for companies).

- KRA PIN Certificate (for the business and possibly individual directors/proprietors).

- National IDs of directors/proprietors.

- Business Bank Account Details: A formal bank account in the name of your registered business.

- Business Permit/License (depending on the nature of your business and local county requirements).

For Freelancers/Small Scale: While some platforms might offer very basic payment links for individuals, these usually come with lower transaction limits and may not scale for a growing business. For serious and sustained online transactions, formal business registration is highly recommended and usually mandatory for full access to a gateway’s features and higher limits. The process for registering a business in Kenya is now largely digitized through the eCitizen portal, making it more accessible.

How do I withdraw money from these platforms to my Kenyan bank account?

The process for withdrawing funds from a payment gateway in Kenya to your local bank account is designed to be straightforward and secure. While specific steps might vary slightly between providers, the general procedure is as follows:

- Login to Your Merchant Dashboard: After successful registration and setup, you’ll be provided with login credentials to your dedicated merchant portal (e.g., Pesapal Dashboard, Flutterwave Dashboard, Paystack Dashboard, DPO Merchant Portal).

- Navigate to the Payouts/Withdrawals Section: Within the dashboard, there will typically be a clearly labeled section for “Payouts,” “Withdrawals,” “Transfers,” or “Settlements.”

- Link Your Kenyan Bank Account: If you haven’t already done so during setup, you will need to add and verify your Kenyan bank account details. This usually involves providing:

- Bank Name

- Bank Branch

- Account Name (must match your business registration name)

- Account Number

- SWIFT/BIC Code (for international banks if you’re receiving foreign currency, though for local KES payouts, your bank usually provides specific routing details).

- Verification: Some gateways may require a bank statement or a cancelled cheque to verify the account ownership.

- Initiate a Withdrawal/Payout:

- You’ll see your available balance (funds that have been processed and cleared for settlement).

- Enter the amount you wish to withdraw.

- Select the linked Kenyan bank account.

- Confirm the transaction.

- Review Settlement Duration: The gateway will typically display the estimated time it will take for the funds to reflect in your bank account. As discussed earlier, this can range from T+1 (next business day) to T+3 or T+5 depending on the gateway and the bank.

Important Considerations:

- Withdrawal Fees: Be aware of any fees associated with withdrawing funds from your gateway balance to your bank account. These are usually small flat fees or a very small percentage.

- Minimum Withdrawal Limits: Some gateways might have a minimum amount you need to accumulate before you can initiate a withdrawal.

- Automated vs. Manual Payouts: Some gateways offer automated daily or weekly payouts, while others require you to manually initiate each withdrawal. Configure this based on your cash flow needs.

By understanding these common questions and their answers, Kenyan businesses can confidently navigate the landscape of online payment gateways, ensuring they make informed decisions that support their growth and operational efficiency in the dynamic digital economy.

uture of commerce in Kenya is digital, and with the right payment partner, your business is set to thrive.

Common Challenges and Solutions for Businesses Using Payment Gateways in Kenya

While the benefits of online payment gateways in Kenya are undeniable, businesses often encounter various challenges during implementation and ongoing operation. Understanding these hurdles and proactively addressing them is crucial for a smooth and effective digital payment strategy.

1. High Transaction Fees and Opaque Pricing Models

Challenge: One of the most persistent frustrations for businesses, especially SMEs, is the perceived high cost of transaction fees and the often complex, non-transparent pricing structures of some payment gateways in Kenya. These fees, whether a percentage, a fixed amount, or a combination, can significantly eat into profit margins, particularly for businesses dealing with low-value, high-volume transactions. Hidden charges, such as setup fees, withdrawal fees, or chargeback penalties, can also lead to unexpected costs.

Solution:

- Thorough Fee Analysis: Don’t just look at the advertised percentage. Request a full, itemized fee schedule from multiple providers. Create a spreadsheet to calculate the total cost based on your projected transaction volume and average value across different payment methods (M-PESA, local cards, international cards).

- Example: For a business expecting 1,000 transactions a month with an average value of KES 500, a 2.5% fee plus KES 10 per transaction would mean KES 25 (0.025 * 500) + KES 10 = KES 35 per transaction, totaling KES 35,000. Compare this rigorously across providers.

- Negotiate: For businesses with significant transaction volumes, don’t shy away from negotiating fees. Many payment gateways in Kenya are open to discussions for enterprise clients.

- Understand Tiered Pricing: Some gateways offer lower rates as your transaction volume increases. Factor this into your long-term cost projections.

- Prioritize Value over “Cheap”: The cheapest option isn’t always the best. A slightly higher fee might be justified by superior security, better customer support, faster settlements, or broader payment method acceptance, which can prevent losses from fraud or improve customer experience.

2. Integration Complexities and Technical Hurdles

Challenge: Integrating a payment gateway with an existing e-commerce website, mobile app, or custom business system can be technically challenging. Issues can arise from poorly documented APIs, compatibility problems with specific platforms (e.g., outdated CMS versions), or a lack of in-house technical expertise. This can lead to prolonged setup times, increased development costs, and frustrating technical glitches.

Solution:

- Utilize Ready-Made Plugins/Extensions: For popular e-commerce platforms like WooCommerce, Shopify, Magento, or Prestashop, prioritize payment gateways in Kenya that offer official, well-maintained plugins. These are designed for ease of installation and minimal coding.

- Assess API Documentation and SDKs: If you have a custom system or mobile app, thoroughly review the gateway’s API documentation and available SDKs (Software Development Kits). Good documentation, code samples, and active developer communities are invaluable.

- Leverage Sandbox Environments: Before going live, use the gateway’s sandbox (testing) environment to simulate transactions and ensure seamless integration without affecting real money. This helps identify and fix issues early.

- Seek Expert Assistance: If in-house expertise is limited, consider hiring a freelance developer or a specialized IT consultancy with experience in payment gateway integration in Kenya. Many reputable web development agencies in Nairobi specialize in this.

3. Security Concerns and Fraud Prevention

Challenge: Online transactions are inherently vulnerable to fraud, cyberattacks, and data breaches. Businesses face the constant threat of chargebacks (when customers dispute transactions), phishing attempts, and other forms of financial crime. Ensuring the highest level of security and compliance (like PCI DSS) can be complex and intimidating for businesses without dedicated cybersecurity teams. Overly aggressive fraud filters can also mistakenly flag legitimate transactions, leading to lost sales.

Solution:

- Prioritize PCI DSS Compliance: Always choose a payment gateway in Kenya that is PCI DSS Level 1 compliant. This offloads much of the burden of handling sensitive card data from your business to the gateway, significantly reducing your compliance scope.

- Enable 3D Secure: Implement 3D Secure (e.g., Verified by Visa, Mastercard SecureCode) for card transactions. This adds an extra layer of authentication, shifting liability for fraudulent chargebacks from you to the card issuer.

- Utilize Gateway Fraud Tools: Leverage the fraud detection and prevention tools offered by your chosen gateway. These often include:

- Address Verification System (AVS) & Card Verification Value (CVV) checks.

- Machine learning-based fraud scoring that analyzes transaction patterns.

- Transaction velocity checks (e.g., too many transactions from one card in a short period).

- Educate Your Team: Train your staff on identifying suspicious orders, phishing attempts, and proper data handling procedures.

- Regular Security Audits: Conduct periodic security audits of your website or e-commerce platform to identify and patch vulnerabilities.

- Be Proactive on Chargebacks: Maintain clear records of all transactions, shipping confirmations, and customer communications. Respond promptly and comprehensively to any chargeback disputes with supporting evidence.

4. Delayed Settlements and Cash Flow Management

Challenge: Delays in receiving funds from processed transactions can significantly impact a business’s cash flow, making it difficult to pay suppliers, manage inventory, or meet operational expenses. While M-PESA settlements are often near real-time, card payments can take longer.

Solution:

- Understand Settlement Times: Before choosing a gateway, clearly understand their typical settlement duration for each payment method (e.g., T+1, T+2, T+3).

- Optimize Payout Schedules: Many payment gateways in Kenya allow you to set your payout schedule (e.g., daily, weekly). Configure this to align with your business’s cash flow needs.

- Maintain a Buffer: Always keep a sufficient cash reserve in your business bank account to cover operational expenses during settlement periods.

- Diversify Payment Options: While M-PESA offers fast settlements, relying solely on it might limit your customer reach. A balanced approach with a gateway that offers quick settlements for cards as well is ideal.

- Utilize Reporting: Leverage the gateway’s dashboard and reporting tools to track incoming funds and monitor your cash flow in real-time.

5. Lack of Localized Support and Understanding

Challenge: Some international payment gateways may offer impressive technology but lack a deep understanding of the unique dynamics of the Kenyan market, including specific M-PESA nuances, local banking practices, or relevant regulatory requirements. This can lead to frustration when seeking support or resolving issues that require local context.

Solution:

- Prioritize Local Presence: Whenever possible, choose a payment gateway in Kenya that has a strong local presence, dedicated support teams based in Kenya, and a clear understanding of the local payment ecosystem. Pesapal is a prime example of a locally strong player.

- Test Customer Support: Before committing, try reaching out to their customer support with a few queries to gauge their responsiveness and helpfulness.

- Community and Reviews: Check online reviews and local business forums to see other Kenyan merchants’ experiences with different gateways, particularly concerning support.

By being aware of these common challenges and proactively implementing these solutions, businesses in Kenya can maximize the benefits of online payment gateways, ensuring a seamless, secure, and efficient payment experience for both themselves and their customers.

Understanding the Regulatory Environment for Payment Gateways in Kenya

Beyond the technical and commercial aspects, businesses leveraging online payment gateways in Kenya must operate within a specific regulatory framework. Adhering to these regulations is not just about compliance; it’s about building trust, ensuring security, and safeguarding both your business and your customers.

The Role of the Central Bank of Kenya (CBK)

The Central Bank of Kenya (CBK) is the primary regulatory authority for the payment systems in the country. Under the National Payment System Act, 2011, and subsequent regulations, the CBK oversees and licenses payment service providers (PSPs), including the operators of payment gateways. Their mandate includes:

- Licensing and Oversight: Ensuring that all entities providing payment services meet specific criteria for financial stability, operational capability, and consumer protection.

- Promoting Stability and Efficiency: Developing policies and standards (like the KE-QR Code Standard 2023) to foster a secure, reliable, and efficient payment ecosystem.

- Consumer Protection: Safeguarding users against fraud, unfair practices, and ensuring transparency in transactions.

- Anti-Money Laundering (AML) and Combating the Financing of Terrorism (CFT): Implementing stringent regulations to prevent the use of payment systems for illicit activities.

When choosing a payment gateway in Kenya, always verify that they are properly licensed by the CBK. Reputable gateways will prominently display their regulatory compliance.

Key Regulatory Requirements and Compliance Standards

Businesses and their chosen payment gateways in Kenya must adhere to several crucial standards and regulations:

- PCI DSS Compliance (Payment Card Industry Data Security Standard):

- Requirement: Any entity that stores, processes, or transmits cardholder data (credit/debit card information) must be PCI DSS compliant. This applies not only to payment gateways but also to businesses that handle card data on their own servers (though reputable gateways help offload much of this burden).

- Importance for Businesses: By using a PCI DSS Level 1 certified payment gateway, your business significantly reduces its own PCI DSS compliance scope. This means you don’t have to invest as heavily in complex security infrastructure to protect card data, as the gateway takes on that responsibility. However, you are still responsible for your own website’s security and how you integrate with the gateway.

- Consequences of Non-Compliance: Non-compliance can lead to hefty fines, reputational damage, increased transaction fees, and even the inability to process card payments.

- Kenya Data Protection Act, 2019:

- Requirement: This Act, modeled on global best practices like GDPR, governs the collection, processing, storage, and sharing of personal data in Kenya. It mandates that any entity (data controller or data processor) handling personal data must register with the Office of the Data Protection Commissioner (ODPC).

- Importance for Payment Gateways: Payment gateways in Kenya process vast amounts of personal data (names, contact details, transaction history, etc.). They must comply with the principles of data protection, including lawful processing, data minimization, accuracy, integrity, and confidentiality. They are typically registered as data processors.

- Importance for Businesses: As a business, you are likely the data controller as you determine the purpose and means of processing customer data. You must ensure that your contracts with payment gateways (your data processors) explicitly outline their data protection obligations and that they are compliant with the DPA. You also need to ensure you have a privacy policy visible to customers.

- Anti-Money Laundering (AML) and Counter-Terrorism Financing (CTF) Regulations:

- Requirement: Both payment gateways and businesses are subject to AML/CTF regulations. This involves robust “Know Your Customer” (KYC) procedures during onboarding (collecting and verifying identity documents), transaction monitoring to detect suspicious activities, and reporting unusual transactions to the Financial Reporting Centre (FRC).

- Importance: These regulations are critical for preventing financial crime. Your business’s compliance, particularly during registration with a gateway, contributes to the overall integrity of the financial system. Failure to comply can result in severe penalties, including fines and imprisonment.

- Consumer Protection Regulations:

- Requirement: Various laws aim to protect consumers in digital transactions, ensuring transparency in pricing, clear terms and conditions, and fair dispute resolution mechanisms.

- Importance: Your chosen payment gateway should facilitate consumer rights, such as easy access to transaction histories, clear refund/chargeback policies, and secure dispute resolution channels. As a business, you must also uphold these principles in your interactions with customers.

Emerging Regulatory Considerations (2025 and Beyond)

- Digital Lending Regulations: With the rise of BNPL and other digital credit services (often integrated with payment solutions), the CBK is increasing its scrutiny and regulation of these entities to curb predatory lending and protect consumers from debt traps. Businesses offering or integrating such services need to stay informed.

- Interoperability: The CBK’s push for greater interoperability (e.g., between mobile money platforms, or across different QR code systems) aims to create a more unified and seamless payment experience. Future regulations may further enforce standards to ensure smooth transactions across various providers.

- Open Banking/Finance Frameworks: While still in early stages, Kenya is exploring concepts of open banking, which could lead to regulations requiring banks to securely share customer data (with consent) with third-party providers. This could unlock new payment innovations.

By understanding and proactively complying with this robust regulatory environment, businesses can not only avoid legal pitfalls but also build a strong foundation of trust with their customers, which is invaluable for sustainable growth in Kenya’s digital economy.

Final Thoughts: Making the Right Payment Gateway Choice for Long-Term Growth

The digital payment landscape in Kenya is not just evolving; it’s a vibrant, fast-paced ecosystem that presents immense opportunities for businesses to connect with customers, streamline operations, and achieve unprecedented growth. In 2025, a business’s ability to thrive increasingly hinges on its strategic embrace of digital payment solutions. Therefore, choosing the right online payment gateway in Kenya is not merely a technical decision but a pivotal business strategy that will directly impact your efficiency, customer satisfaction, and ultimately, your profitability.

The Future of Digital Payments in Kenya: Trends to Watch

As you finalize your choice, it’s beneficial to cast an eye on the emerging trends shaping Kenya’s digital payment future:

- Continued Mobile Money Dominance: M-PESA will remain the king, but expect increasing interoperability between different mobile money platforms and deeper integration into everyday services. The Central Bank of Kenya’s National Payments Strategy 2022-2025 aims to foster a “secure, fast, efficient, and collaborative payments system that supports financial inclusion and innovations,” with a strong emphasis on interoperability.

- Rise of “Phygital” Experiences: The blend of physical and digital payments will become more seamless. Think QR code payments at physical stores, tap-to-pay (NFC) with mobile phones, and embedded finance where payment options are integrated directly into non-financial platforms or apps. Businesses should prepare for solutions like “SoftPOS” (e.g., Tumatap by Interswitch) that turn smartphones into payment terminals.

- Real-time Payments as the New Standard: Consumers and businesses increasingly expect instant transactions. The push for faster settlement times will continue, driven by enhancements like the extended operating hours of the Kenya Electronic Payment and Settlement System (KEPSS) to 7 AM to 7 PM. This will improve cash flow for businesses across the board.

- Enhanced Security and AI-Powered Fraud Prevention: As digital transactions grow, so do cyber threats. Payment gateways in Kenya are investing heavily in AI and machine learning to detect and prevent fraud in real-time. Expect more sophisticated biometric authentication methods and continuous adaptation to new fraud tactics. Businesses must prioritize gateways with robust fraud management tools.

- Growth of Buy Now, Pay Later (BNPL): This flexible payment option is gaining significant traction globally and in Kenya, particularly among younger, tech-savvy consumers. Integrating BNPL options can boost sales and cater to evolving consumer spending habits.

- Open Finance and API-driven Innovation: The payments ecosystem will become more collaborative, with traditional banks partnering with fintechs to offer innovative services. This open approach, driven by robust APIs, will enable businesses to create more tailored and integrated payment experiences.

- Potential for Central Bank Digital Currency (CBDC): While still in exploratory phases, the Central Bank of Kenya is looking into a digital Kenyan Shilling. If implemented, a CBDC could lower transaction costs and offer a government-backed digital currency, potentially reshaping the payment landscape significantly in the long term.

Actionable Advice for Making Your Final Choice

To make the best decision for your business, consider these actionable steps:

- Define Your Needs Clearly:

- Customer Base: Are your customers predominantly local (M-PESA heavy) or international (card/PayPal heavy)?

- Transaction Volume & Value: How many transactions do you anticipate, and what’s their average value? This impacts fee structures.

- Business Model: Are you e-commerce, services, subscriptions, or a physical store?

- Technical Capability: Do you have developers for API integration, or do you need simple plugins?

- Conduct a Detailed Cost Analysis:

- Go beyond the advertised per-transaction fee. Calculate the total cost including setup, monthly, withdrawal, and potential chargeback fees based on your projected transaction mix.

- Ask for a customized quote for your specific business size and type.

- Prioritize M-PESA Integration (It’s Non-Negotiable in Kenya):

- Ensure the gateway offers robust, reliable, and user-friendly M-PESA support (ideally with STK Push). This is paramount for the Kenyan market.

- Verify Security & Compliance:

- Always choose a payment gateway in Kenya that is PCI DSS compliant and has strong fraud prevention tools. Ask about their data protection protocols in line with Kenya’s Data Protection Act, 2019. Your customers’ trust depends on it.

- Test Integration & User Experience:

- If possible, utilize sandbox environments to test the integration with your platform.

- Evaluate the customer checkout experience: Is it smooth, fast, and intuitive? A clunky checkout leads to abandoned carts.

- Assess Customer Support and Reliability:

- Look for responsive customer support, ideally with local presence or understanding of Kenyan payment nuances.

- Inquire about their uptime history and dispute resolution process.

- Consider Scalability:

- Choose a payment gateway that can grow with your business. You don’t want to switch providers every time your transaction volume increases or you expand into new markets.

By meticulously evaluating these factors and aligning them with your business goals, you’ll be well-equipped to select an online payment gateway in Kenya that not only meets your current needs but also strategically positions you for long-term success in this dynamic and exciting digital economy. The f